I am positive on Spotify’s Q3 2024 earnings. My estimates takes into account the price changes during the quarter, competitive positioning, cost efficiencies and quality of its products among others. Here is a description of my bullish points:

- Price increases: On June 2024, Spotify increased monthly subscriptions by an average of 8.5%. In the Q2 2024 earnings call, CFO Ben Kung said this price increase will contribute 100 to 200 basis points to the average revenue per user (ARPU) growth in Q3. As such, I expect the price increase to be the primary contributor to revenue growth in Q3.

- More pricing options: On June 2024, Spotify introduced a basic plan tier in the U.S. priced at $10.99 per month. This came three months after Spotify introduced an audiobooks tier in the U.S. priced at $9.99 per month. This additional options enables them to convert free users who are only interested in either music streaming or audiobooks at a lower price compared to the standard premium option. Deutsche Bank expects the audiobooks tier to contribute 80 basis points to the quarter-over-quarter growth in premium gross margins in Q3.

- Great product offering: According to analysts, Spotify has the best-in-class product offering. This can be seen from the great reception of its new products such as AI Playlist and Spotify Daylist. Spotify’s great products help the company to negotiate reduced payments to labels and to incur less churn when it increases prices.

- Competitive position remains solid: An August survey by Evercore established that Spotify continue to lead the music streaming industry in the U.S and U.K and that this lead keeps growing. The lower pricing of its monthly plans enables Spotify to remain competitive against the likes of YouTube. For instance, Jefferies estimates that Spotify’s pricing is significantly less than that of YouTube in 15 key markets.

- Bundling of subscriptions: In March 2024, Spotify announced that it was going to to reclassify its Premium Individual, Duo, and Family subscription plans as Bundled Subscription Offerings because they now have audiobooks. This enabled Spotify to cut costs in Q2 by $35 million. As Spotify bundles the subscription in other regions, the cost-savings increases. Mechanical Licensing Collective (The MLC) filed a legal suit against Spotify for doing this. However, I believe that Spotify will win the case since their 2022 legal settlement gives Spotify the right to do this.

- Focus on profitability: Since last year, Spotify has been focusing on profitability. This means that operating costs are not expected to rise significantly in the near-term.

- Netflix Q3 2024 results: Netflix Q3 2024 results topped analysts estimates indicating that consumers are still spending on entertainment despite the macro headwinds.

Headwinds during the quarter include:

- Social charges and currency fluctuations: Social charges is the main headwind that could impact Spotify’s operating income during the quarter. For instance, the management guided operating income of $405 million at a time when Spotify’s share price was trading at $313.79. Spotify’s shares ended Q3 2024 at $375. In Q2, the company reported social charges that were $47 million higher than expected (page 3) after the stock appreciated by $50 million during the quarter. As such, I expect the Q3 social charges to be around €45 million higher than the guided €15 million. Currency fluctuations could also impact the results during the quarter.

- Missed MAU guidance in the last three quarters: Spotify has missed its MAU guidance in the last three quarters by an average of 3 million. This may suggest that the churn associated with price increase last year may have come in higher than expected by the management. The same thing could happen when Spotify reports its Q3 results.

- Top-funnel spending remains volatile: Spotify said in its Q2 earnings call that ad spending in the upper funnel remains volatile. It also said that they are swiftly converting higher-engaged users to premium subscription. As such, I don’t expect ouperformance in its ad business in the near term.

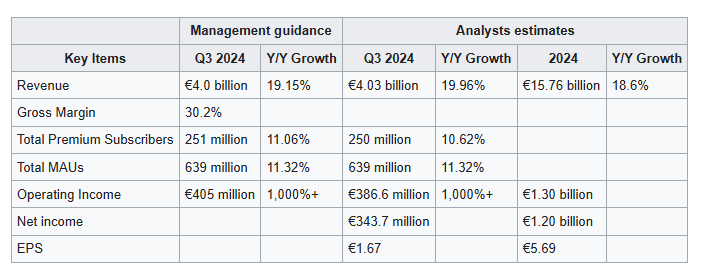

Here are the analysts and management expectations:

My estimates for 2024 include revenue of €15.74 billion (+18.9%), net income of €1.27 billion, and EPS of €5.70.