This topic discusses the upcoming United Internet Q2 2025 earnings, including our outlook and a summary of the results. You can find our full Wiki article here:

Earnings date: August 7, 2025

Time of Earnings release: 7:30 CET

Time of 1&1 Analysts Call: 1:00 PM CEST

Time of United Internet Analysts Call: 2:30 PM CEST

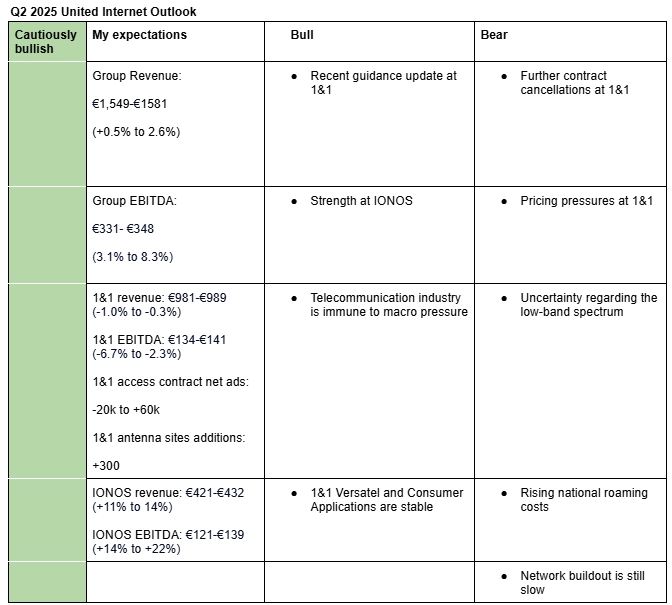

I am cautiously bullish on United Internet’s Q2 2025 earnings. I expect strength at IONOS to largely offset weakness at 1&1, which continues to face competitive pressure and churn related to network migration. My estimates also reflect the resilience of the broader industry. However, the share price could come under pressure from near-term headwinds at 1&1 such as uncertainty around the low-band spectrum, possibility of a slower-than-expected network buildout, and management commentary on rising national roaming costs.

Given the upsides described at Notion, I reiterate a buy/hold rating on the United Internet shares. Here is a description of my bullish and bearish factors.

Bullish factors

Recent guidance update at 1&1: On June 27, 1&1 reiterated its service revenue guidance for 2025 (flat growth). 1&1 contributes 64% revenue to United Internet and the guidance update signals limited downside risk to revenue in Q2 2025.

Strength at IONOS: IONOS’s operating performance is currently the bright spot at the group. I expect the strength at IONOS to fully compensate revenue and EBITDA decline at 1&1 in Q2 2025. IONOS contributes around 25% revenue and 33% EBITDA to United Internet. Together, IONOS and 1&1 contribute 89% revenue and 79% EBITDA to United Internet.

1&1 Versatel and Consumer Applications are stable: 1&1 Versatel and Consumer Applications (GMX and WEB.DE) are showing stable revenue and EBITDA growth trends. United Internet continues to make investments in Consumer Applications that should boost their EBITDA margin in the near-term.

Industry is immune to macro pressure: The telecommunication industry is largely immune to macro pressure since people cannot do without calls or mobile data. Similarly, United Internet’s business is largely non-cyclical. Therefore, the slowdown in Germany’s economy is unlikely to have much impact on United Internet’s operating performance.

Bearish factors

Further contract cancelation at 1&1: 1&1 expects continued churn as a result of customer migration from O2 network to own network until the end of 2025.

Pricing pressure at 1&1: Competition in Germany’s telecommunications market remains intense. Commentary from Vodafone’s and O2’s earnings calls indicates that pricing pressure persisted into Q2. As a result, I do not expect average revenue per user (ARPU) to grow at 1&1 during the quarter.

Uncertainty regarding the low-band spectrum: 1&1 and the incumbent operators are expected to reach an agreement by January 2026. However, with the year already halfway through and no progress publicly disclosed, uncertainty around the outcome is rising. A recent draft by Deutsche Telecom calling for the "establishment of flexible ‘use it or share it or trade it or lose it’ conditions and frequency trading" may signal resistance to share the low-band frequency with 1&1. O2 also signaled in May resistance to share it. A delay in securing access to low-band spectrum would force 1&1 to rely more heavily on national roaming, prolonging elevated network operating costs and delaying margin improvement.

Rising national roaming costs: On June 27, 1&1 lowered its 2025 EBITDA guidance by €26 million, citing higher than expected national roaming costs driven by increased usage of Vodafone’s network. This elevated usage may be due to limited coverage from 1&1’s own infrastructure, raising the risk that roaming costs could increase further in the near term as the network buildout remains in its early stages.

Network buildout is still slow: Antenna site rollout at 1&1 remains slow. As of last quarter, the company had only 1,000 active sites (unchanged from Q4 2024), yet it needs 6,000-6,500 by the end of 2025 to meet its 25% population coverage obligation. Failure to meet this target could result in regulatory penalties, similar to the 2022 shortfall, which carried fines of €50,000 per missing site (yet to be imposed).

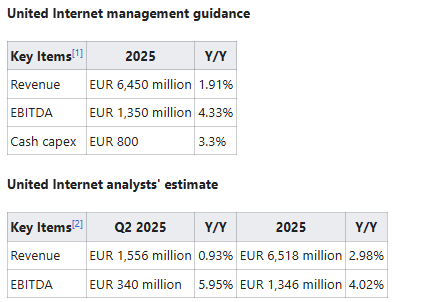

Here are analysts estimates and management guidance for Q2 2025 and FY2025:

United Internet topped revenue estimates in Q2, reported EBITDA roughly in line with expectations, and maintained its 2025 outlook

United Internet’s Q2 2025 revenue rose 4.2% y/y to €1,606 million (calculated based on H1 unadjusted results), above analysts estimate of €1,556 million, while EBITDA rose 4.2% y/y to €334 million, slightly below analysts estimate of €340 million.

United Internet reiterated its 2025 outlook which includes service revenue of approximately €6.45 billion (Analysts estimate: €6,518 million ), EBITDA of approximately €1.35 billion (Analysts estimate: €1,346 billion) and cash CapEx of around €800 million (2024: €774.6 million).

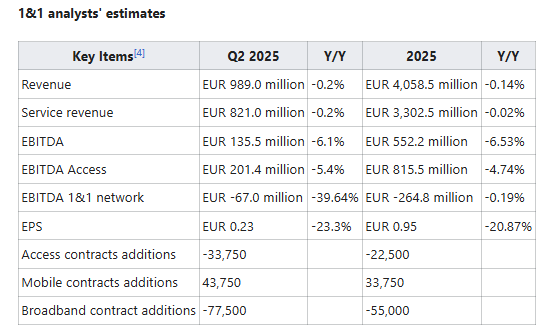

1&1’s Q2 2025 revenue was flat y/y at €988 million (in line with estimates), EBITDA fell 11.3% y/y to €128.0 million (analysts estimate: €135.5 million), EBIT declined 43% y/y to €44.9 million (analysts estimate: €54.9 million), EPS was €0.15 (analysts estimate: €0.23) while access contracts were flat y/y at 16.33 million (analysts estimate:16.32 million).

1&1 reiterated its 2025 guidance given in June which includes EBITDA of approximately €545 million (previous guidance: 571 million), EBITDA in access segment of around €810 million (2024: €856.1 million), 1&1 network EBITDA of approximately -€265 million (2024: -€265.3 million) and cash capex of around €450 million (2024: €290.6 million).

1&1 said 1,200 antenna sites are now active, up from 1,000 at the end of Q1 2025, 4,500 are under development and that Vantage Towers continue to underdeliver (page 5).

United Internet said its stake in 1&1 is now 85.10%, after acquiring additional 4.29% through the voluntary public tender offer (page 14).

Assessment

Even when adjusted for the discontinued energy division, revenue is up 4.3% y/y to €1,600 million while EBITDA is up 4% y/y to €333 million. United Internet shares are now down 2.6%, probably due to the slight miss in EBITDA or the slight miss in revenue outlook.

Overall, I think the results were solid, aided by strength at IONOS.

I don’t like that 1&1’s network progress is still slow. At 1,200 active antenna sites, hitting the 6,000-6,500 target is now nearly impossible.

How do the 1,200 active antenna sites compare to our projections?

How do the 4,500 sites under development compare with sites under development from the quarters before and our expectations?

Do we have a Notion page in which we track all of this + have projections?

I don’t normally estimate the number of active antenna sites given that 1&1 can even go for three months before adding more.

Last quarter, it said it had 5,000 antenna sites under development. Based on this, we can assume 1&1 developed 500 sites ( actives: 200, Inactive: 300). However, my math could be wrong given that the partners are likely to have brought additional sites under development. I expected 1&1 to add a total of 300 sites in the quarter, given management has consistently said they are adding 200-300 sites per quarter.

I think it would be a good idea to estimate them so we can always quickly see how they are doing compared to our estimates. (A very important element of all our formats is ease of use so we instantly see everything relevant and get reminded on key numbers - this way we can create an persistent overview of what is important because otherwise it’s impossible to remember everything)

I like the table in the linked Notion page. Maybe we can link that page in the future and extend it a bit. (Future projection + adding sites under development or anything else that makes it even better)

Here are the main insights from the United Internet and 1&1 earnings calls;

1&1 has build a total of around 5,800 antenna sites in the pipeline; 1,200 active sites, 2,300 built but offline, and 2,300 in progress or contracted (min 44:00, 1&1 Call).

Dommermuth said 1&1 has not yet received an offer for the low-band frequency and expects competitors to delay the process as much as possible, adding that the timing will depend on intervention by BNetzA (min 33:00, 1&1 Call).

Dommermuth said if the Vodafone network grows more slowly than expected, they will have to buy more capacity from Vodafone (min 6.40, 1&1 Call)

Competition in the mobile market remains intense, with Telefónica’s sharp price cuts a few months ago prompting rivals to consider their response (min 51:18, 1&1 Call).

Currently, customers who switch to Vodafone’s network cannot return to 1&1, but this will soon change, reducing national roaming costs (min 47:23, 1&1 Call).

Dommermuth said that if offered additional 1&1 share packages they would purchase them, but they do not plan to buy shares on the stock exchange, and their current plan does not include a squeeze-out (min 53:01, 1&1 Call).

Dommermuth said they don’t plan to sell any of the businesses, pointing out that they have a good portfolio that compensates each other (min 24:34, United Internet Call).

Assessment

At 2,300, the number of inactive base stations has improved, implying that 1&1 added roughly 500 sites per quarter. If this pace continues, the total base station count could reach around 5,100-5,800 by the end of 2025.

The rollout of active base stations, however, remains slow. At the current rate, I estimate 1&1 will have only 2,000-2,500 active sites by year-end, well below the 6,000-6,500 target. Management still maintains it can achieve 25% coverage by year-end, suggesting they expect a significant acceleration in execution in the second half. I believe Q3 performance will be the key test of whether this target is realistic.

Overall, while risks related to national roaming costs and low-band frequency persist, I remain optimistic about cost savings next year, driven by €100 million in savings from customer migration, efficiencies from two-way roaming handovers, and cost savings from international roaming.