Meta’s Q2 surges past estimates; 2026 expenses and CapEx set to stay elevated

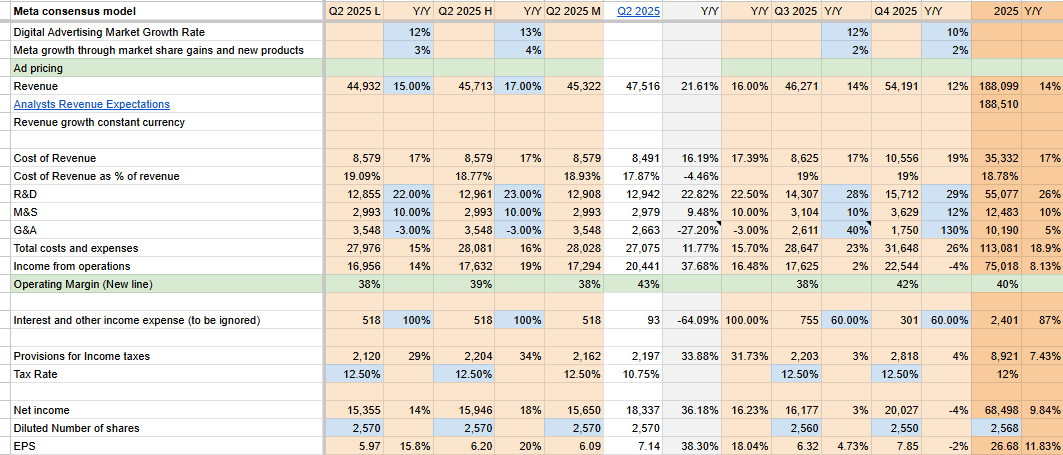

- Meta Q2 2025 revenue rose 22% y/y to $47.5 billion, above management’s upper guidance of $45.5 billion and analysts estimate of $44.8 billion, EPS came in at $7.14 versus analysts estimate of $5.89 while operating margin of 43% exceeded analysts estimate of 38%.

- Family daily active people (DAP) rose 6% y/y to 3.48 billion, versus analysts estimate of 3.45 billion, ad impressions grew 11% y/y (Q1 2025: +5%) while average price per ad increased 9% y/y (Q1 2025: +10%).

- Meta is guiding Q3 2025 revenue in the range of $47.5-50.5 billion (analysts estimate: $44.62 billion)- which assumes FX tailwind of 1%, 2025 total expenses in the range of $114-118 billion (increased from $113-118 billion) and CapEx in the range of $66-72 billion (increased from $64-72 billion).

- Meta expects 2026 y/y expense growth rate to be higher than the 2025 expense growth rate driven by infrastructure costs and employee compensation.

- It expects 2026 to be another year of significant capital expenditure as it continues increasing capacity to support AI and business operations.

- Meta continues to flag EU’s DMA, pointing out that it could significantly impact its business as early as Q3.

Assessment

This was another strong quarter for Meta. Q2 2025 revenue grew 22% year-over-year, exceeding my upper estimate of 17%. Cost of revenue, R&D, and Sales & Marketing expenses were in line with expectations, while G&A came in $900 million below my estimate. Q3 2025 revenue guidance also topped my forecast of $46.3 billion.

There were no one-off benefits during the quarter, and FX impact was neutral.