This topic discusses the upcoming Q2 2023 Upwork Earnings. (Chart)

It will include our final assessment and decision before the earnings release, report on the results, and discuss the results including any potential changes to my position.

Even though Upwork is still the fourth largest position in the portfolio (but only by a tiny margin following the recent rebound) Upwork earnings rank regularly in the Top 3 most relevant earnings given their volatile nature and are the second most important earnings this quarter.

After large position increases in the $7-8 range I am now considering if I should take some profits on those buys or if I feel safe enough to hold the entire position for the long run.

More about the investment thesis can be found here.

The work which we are doing specifically in preparation to the earnings can be found in the Wiki.

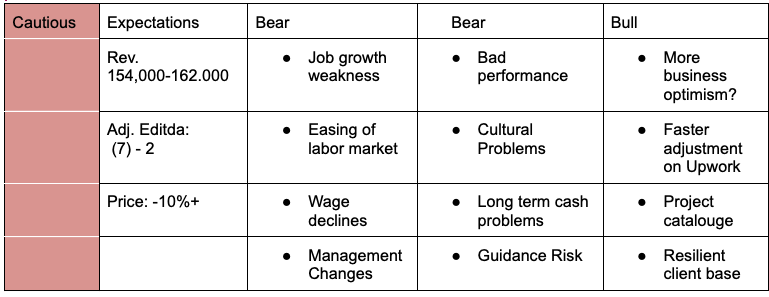

Our expectation for Q2 2023 Upwork Earnings is bearish/cautious.

GSV

We suspect there is a high likelihood that Upworks Plattform Volume called “Gross Service Value” or GSV is going to decline. It appears like this is currently not sufficiently forecasted by management.

There are important data points were are seeing currently that we consider concerning

Jobs posted on Upwork decline slightly during the quarter, but remain mostly on a stable level

Labor markets are also easing, with job posting in a declining trend

We are starting to experience wage pressures to the downside in the economy, which has been experienced inside Upwork too and could persist. This trend is expected to continue, even in a soft landing scenario.

Management

There have been several management changes recently, and the majority of key roles are new. This leads us to believe there could be some cultural problems that disincentive the long term stayed in the company

We are also unsure about the performance that a completely new team could have, especially in challenging times and we witnessed problems in multiple departments ranging from development to sales, to marketing, to financial control.

Cash

Upwork cash is currently only 500M, if the burn rate increases at some point due to a challenging macro, we are unsure of their ability to raise debt in that environment, creating potential cash flow problems. A major 350M loan has to be repaid in 2026.

Upside Surprise

On the upside, there is a possibility that the increase in businesses optimism lately along with a reported resilient client base, and the potential for Upwork clients to have adjusted faster to the economic uncertainty due to its flexibility. They could be therefore ahead of the curve when it comes to cost cuts- This could create a scenario where GSV started to increase again in Q2 2023, beating the current expectations.

Additionally, some of Upworks’s client base might be resilient given that Freelancers are core to many Client Businesses according to Upwork.

The project catalog is making some progress.

Mindmap

We created a draft mindmap with all arguments here.

Summary

Overall we believe that this quarter’s earnings hold a significant risk of missed potential and we get increasingly cautious about the management performance of Hayden Brown after massive leadership changes and internal problems.

I am therefore reducing my position. (Already reduced 28%, considering further reductions)

Fiverr announced its Q2 2023 earnings results today. Here is a summary of the main insights;

Revenue grew by 5.1% y/y to $89.4 million versus management mid-point guidance of $89 million(+5% y/y), driven by growth in spend per buyer and increase in take rate.

Spend per buyer grew 2% y/y to $265 in the 12 months ended June 30,2023. Fiverr expects spend per buyer to increase in the second half of the year.

Its Q2 2023 adjusted EBITDA was $15.3 million versus $13 million guided by management.

Fivver raised its 2023 revenue outlook to $358.0 - $365.0 million from $355.0 - $365.0 million.

It also raised its 2023 adjusted EBITDA guidance to $56.0 - $60.0 million from $48.0 - $56.0 million

I have been thinking that we could have missed that even if the macro and labor picture have not changed, or it’s even easing. If Upwork loses jobs or small clients but is able to attract some fewer clients, but whose spend is able to offset those losses, they can still grow in this environment.

However, I am not sure how sustainable that can be in a more challenging or soft environment.

We also have no way to know probably this is the case quarter by quarter.

I think it‘s always good to reflect on each quarter and the question what we might have missed or what could be improved next quarter.

I think this quarter demonstrates very well how valuable it can be to develop a framework with proprietary data, correlations, reports that serve as indicators etc. that helps us to predict key data points like GSV.

If this is possible and how close we can get to an accurate description of reality is questionable but I think at least we should try.

As an example data from Tinuiti proved to be very valuable and reliable when it comes predicting Meta results. Additionally this kind of data from Tinuiti is not known to the wider market and provides us with an edge.

In my opinion Upwork will have a lot of room to grow and is still early in its adoption cycle from clients. (Given the company and it‘s products don’t change for the worse)

Therefore when thinking about GSV we always have to weigh demand from additional clients (cohorts) and churn/ changes in existing client behavior.

Ultimately what might have helped in my opinion could be more client optimism and spend on freelancers due to a more positive economic outlook.

Additionally some of the weakness from startups esp. in Europe could have eased and without this headwind and consistently new clients coming in (although currently at lower levels) GSV growth q/q might have been easier.

Here are the main insights from the earnings call;

Compared to Q1, they did not see any changes in terms of how clients are navigating the macro environment. Also, updated revenue guidance does not contemplate any changes to the macro environment.

Raised revenue guidance due to the success of its simplified pricing structure and other monetization improvements and they expect GSV to be pretty much steady during the remainder of the year due to lapping of strong quarters.

The changes they made in Q1 led to an improvement in sales team execution; revenue per account manager was up 100% q/q while productivity in the land team was up 13% q/q, with only one month operating under the optimized model.

They are witnessing a little bit of movement by clients to lower priced categories; one of their enterprise clients moved to managed service contract in Q2.

Growth in active clients was driven by 4% y/y increase in retained clients, partially offset by flat growth in new clients.

They are seeing strong trends in generative AI category; wages for generative AI jobs are 50% more than that of other jobs in the marketplace, AI job posts grew 10x sequentially while AI searches was up 15x, but the numbers are coming off from a small base and their GSV contribution is small.