Not sure if analysts have a bias to reduce estimates during the quarter, this way companies can beat them more easily. But seems to be the normal thing to do.

It also tells me just have wrong analyst models are just from 1 quarter to the other. I probably would not trust their estimates at all, unless very few days in advance to earnings.

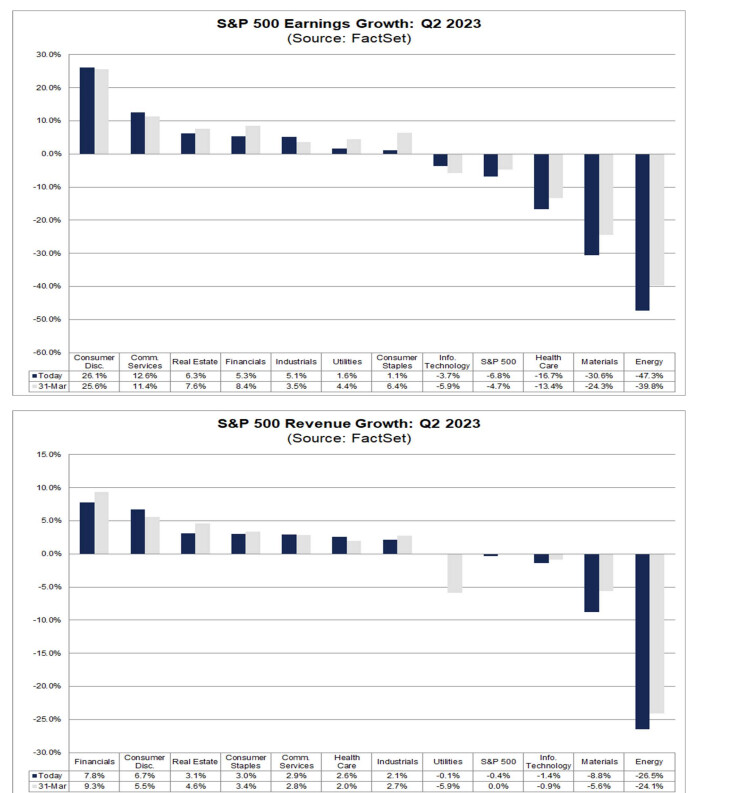

Key Insights July 7 2023 Report:

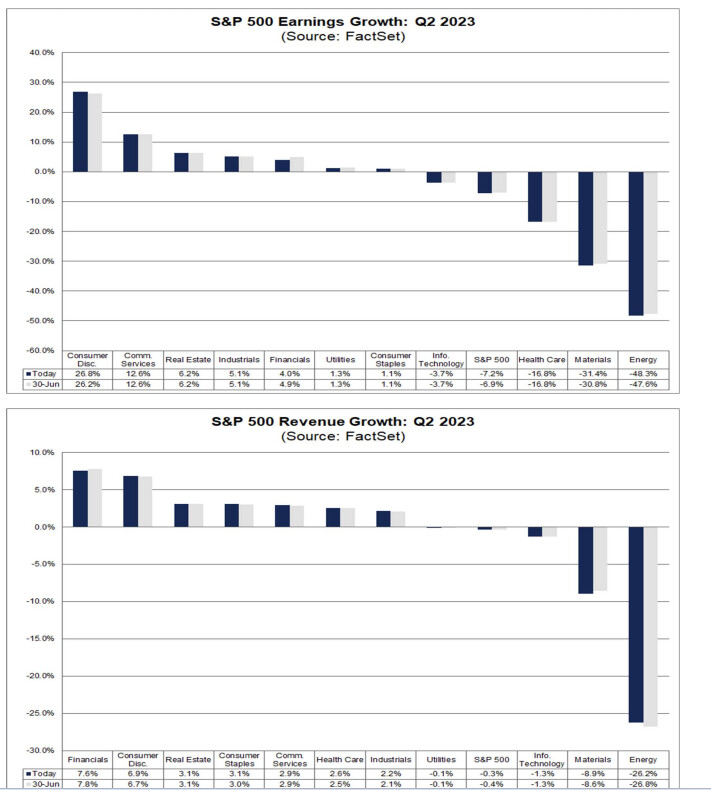

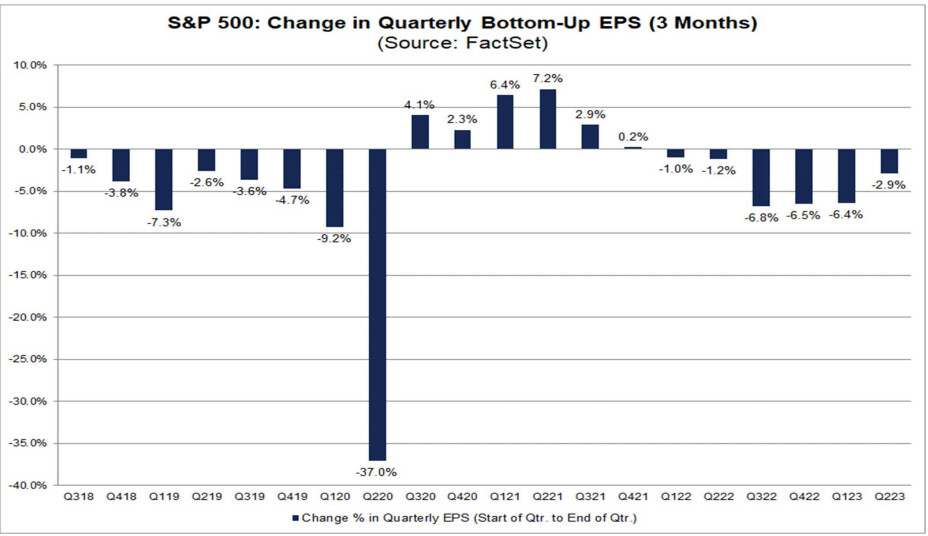

If -7.2% is the actual decline for the quarter, it will mark the largest earnings decline reported by the index since Q2 2020 (-31.6%). It will also mark the third straight quarter in which the index has reported a (year-over-year) decrease in earnings.

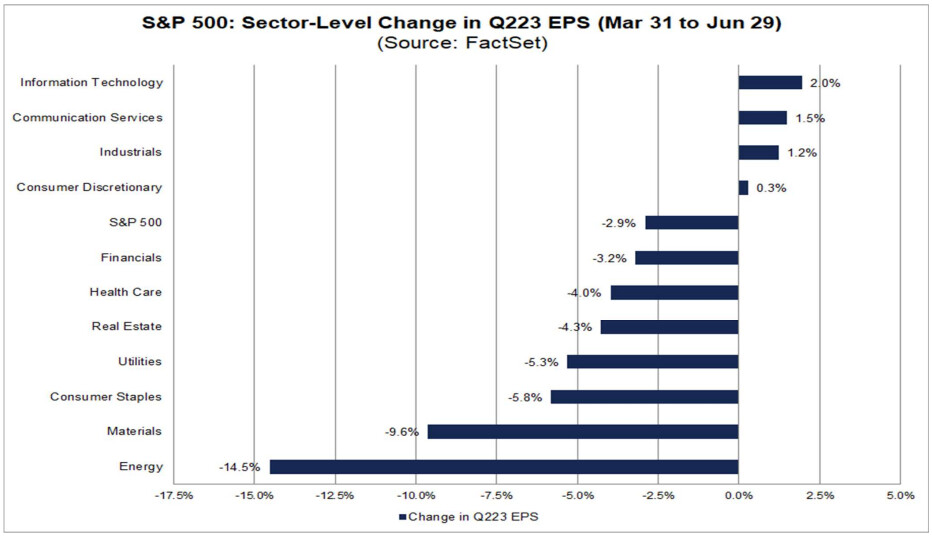

In terms of estimate revisions, analysts lowered earnings estimates for Q2 2023 by a smaller margin than average during the quarter. On a per-share basis, estimated earnings for the second quarter decreased by 3.0% from March 31 to June 30. This decrease is smaller than the 5-year average of -3.4% and smaller than the 10-year average of -3.4%.

In terms of revenues, analysts have also lowered their estimates during the quarter. As of today, the S&P 500 is expected to report a (year-over-year) revenue decline of -0.3%, compared to the expectations for flat revenues (0.0%) on March 31.

The estimated net profit margin for the S&P 500 for Q2 2023 is 11.4%, which is equal to the 5-year average of 11.4%, but below the previous quarter’s net profit margin of 11.5% and below the year-ago net profit margin of 12.2%.

The percentage of S&P 500 companies issuing negative EPS guidance for Q2 2023 is 59% (67 out of 113), which is equal to the 5-year average of 59% and below the 10-year average of 64%.

The forward 12-month P/E ratio is 18.9, which is above the 5-year average (18.6) and above the 10-year average (17.4)

My take:

From what I have read it seems analysts are not pricing at all or taking into account an economic downturn in earnings estimates going forward, and that’s why according to them the bottom in earnings will be already in Q2 2023.

Since I still see a mild recession or at least flat economic growth as the most likely scenario, I am not that confident those estimates are realistic to be honest. And imo could be dangerous too for the markets in the future if they come to the realization that they overestimated the recovery. Especially because we know large revisions are very common.

And as Morgan Stanley pointed out, there will be companies that could realistically benefit from AI short term that will be the exception, but I don’t think this can be true for the whole market.

Factset:

“At the company level, Amazon.com, Meta Platforms, Alphabet, and NVIDIA are expected to be the largest contributors to earnings growth for the S&P 500 for Q4 2023. Amazon.com, Meta Platforms, and NVIDIA are expected to report year-over-year EPS growth of more than 100% in Q4 2023. In addition, analysts have increased EPS estimates for all four companies for the fourth quarter since December 31. If these four companies were excluded, the estimated earnings growth rate for the S&P 500 for Q4 2023 would fall to 4.2% from 8.2%.” What is Driving the Expected Rebound in S&P 500 Earnings Growth in Q4 2023?

Morgan Stanley:

U.S. strategists expect a meaningful earnings recession of -16% for 2023 and a significant recovery in 2024.

Strategists expect falling inflation could hurt margins and that investors are overly optimistic about the positive impact of AI.

Investors should be cautious of looking past 2023 downside and ahead to the potential 2024 rebound given current valuations.

" Investor assumptions on impacts of Fed policy and areas of accelerated earnings growth amid a broader market downturn are now built into consensus expectations, and we respectfully disagree. We think this consensus view stems mostly from some large companies sounding more optimistic about the second half of this year combined with the newfound excitement around artificial intelligence (AI) and what it means for both growth and productivity.

While individual stocks will undoubtedly deliver accelerating growth from spending on AI this year, we don’t think it will be enough to change the trajectory of the overall cyclical earnings trend in a meaningful way. Instead, it may pressure margins further for companies that decide to invest in AI despite flat or slowing top-line growth in the near term."

Yardeni:

He based his projections on a soft landing assumption. Which I think is the majority of analysts’ position at the moment and the reason for the optimistic view on earnings.

The consensus estimate on Wall Street is for earnings-per-share to drop 8.9% year over year in the second quarter, but after big banks kicked off the second quarter earnings season with a strong showing last week, Yardeni sees S&P 500 earnings declining just 4% from a year ago.

" Yardeni expects S&P 500 earnings to hit $270 per share by 2025, and for the blue-chip index to trade between 17.8 and 20 times forward earnings by the end of 2024. For reference, the 10-year average forward price-to-earnings ratio for the S&P 500 is 16.9, and Wall Street’s consensus earnings estimate for 2025 is $275 per share so these aren’t outlandish forecasts."

BNY Mellon:

" Monetary policy has operated with an historical lag of 12-24 months on the real economy. If a recession occurs in 2023, then this year’s EPS could be down as much as 10-20% year-over-year from 2022. In this case, the base from which 2024 earnings grow will be lower, although earnings growth re-acceleration in 2024 could be higher given easier comparisons.

If economic activity holds up in 2023 and a recession is delayed until next year, then 2024’s consensus outlook of 12% EPS growth to $248 is probably too high."

Cool thanks. Pretty good overview of different opinions and how different industries are developing in the Wiki.

Personally I am also skeptical about strong growth in Q4 as I am not sure where it should come from as the Fed is doing it‘s best to slow down the economy.

Even a 10%-20% S&P 500 EPS decline would not alter the investment thesis of my portfolio significantly (obvs. dependent how much individual companies are affected) therefore current scenarios increase my confidence about operating in a relatively stable environment overall.

Basically that all those different scenarios that you quoted look fine to me.

When it comes to the macro environment it is often more important to me that it is relatively stable compared to a strong prediction of growth, which can still happen at an individual company level.

Macrostrength certainly helps, but most investment cases are not constructed around it and do not rely on it.

Even the worst quoted scenarios like an EPS contraction of 20% on an S&P 500 level still falls into the category of relatively stable esp. if some degree of recovery is expected after that.

Taking a longer-term view we still see a strong economy at least for the largest 500 listed companies in the U.S.

So i basically take those scenarios as slightly positive, obvs. without relying too much on them and without changing my assessment that we need to stay vigilant to catch any more drastic deterioration early.