This topic discusses the upcoming United Internet Q1 2026 earnings, including our outlook and a summary of the results. You can find our full Notion article here:

Earnings date: May 12, 2026

Time of Earnings release: 7:30 CET

Time of 1&1 Analysts Call: 10:30 am CET

Time of United Internet Analysts Call: 12:00 PM CEST

Time of IONOS Analysts Call: 09:00 CET

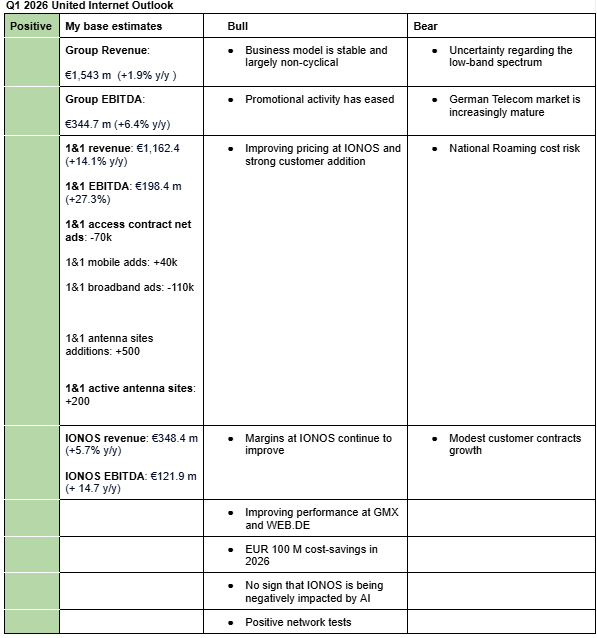

I am positive on United Internet’s Q1 2026 earnings. I expect both the Q1 results and 2026 guidance to come in largely in line with analysts’ estimates. My estimates (United Internet Valuation Model (Google Sheets)) take into account modest growth in 1&1 mobile contracts, easing promotional activity, improving pricing and margins at IONOS, expected cost-savings at 1&1, and the non-cyclical nature of the business. Here is a description of my bullish and bearish arguments.

Bullish arguments

Business model is stable and largely non-cyclical: United Internet has consistently maintained (page 90) that its business is non-cyclical and its performance during times of macro uncertainty confirms it. Additionally, business segments such as GMX and Web.De have stable revenue growth while 1&1 Versatile continues to expand.

Promotional activity: 1&1, Vodafone and Deutsche Telecom indicated in their most recent earnings calls that promotional activity has eased (Q4 2025 United Internet Earnings (Notion)). This supports some pricing growth at 1&1.In fact, 1&1 pointed out that they are planning to increase prices moderately.

Improving pricing at IONOS and strong customer addition: Pricing at IONOS started improving sequentially last quarter and customer addition momentum remains strong (Q4 2025 United Internet Earnings (Notion)).

Margins at IONOS continue to improve: Margins at IONOS continue to improve, offeseting 1&1 network costs. For instance, EBITDA margin improved by almost 4% in Q4 2025 (United Internet Valuation Model (Google Sheets)).

Improving performance at GMX and WEB.DE: According to Ralph Domermuth, Consumer Applications (GMX and WEB.DE) is growing very well (Q4 2025 United Internet Earning (Notion)). During Q4 2025, its revenue rose by 15% y/y while EBITDA margin expanded by 0.6%.

EUR 100 m cost-savings in 2026: 1&1 expects to save EUR 100 M in 2026 which was associated with customer migration from Telefonica Deutschland to own network in 2025 (page 7).

Positive network tests: Third-party tests of 1&1’s network have been very positive (forum post). As such, I don’t expect any major customer churn following the completion of customer migration from Telefonica Deutschland to its own network at the end of 2025.

No sign that IONOS business is being impacted by AI: Investors have been very concerned that AI could take over IONOS’s business. However, last quarter earnings commentary eased these concerns and so far there is no sign that AI is negatively impacting it (Q4 2025 United Internet Earnings (Notion)).

Bearish arguments

Uncertainty regarding the low-band spectrum: The low-band spectrum is crucial for 1&1’s expansion because it provides better indoor coverage and wall penetration. Without it, 1&1 would need to rely more heavily on National Roaming, which is more expensive and therefore limits the upside of owning its own network. According to 1&1, BNetzA is expected to make a decision during spring 2026 (Q4 2025 United Internet Earnings (Notion)). However, based on past precedents, there remains a risk that the decision could be delayed further.

German Telecom market is increasingly mature: Incumbents pointed out in their latest earnings that the German telecom market is increasingly mature (Q4 2025 United Internet Earnings (Notion)). As a result, strong growth at 1&1 through new contracts is unlikely in the near-term unless their is consolidation or OPEN RAN leads to material market share gain.

National Roaming costs risk: 1&1 National Roaming agreement with Vodafone is designed in such a way that if 1&1’s customer contracts grow faster than that of Vodafone, 1&1 will end up paying higher costs than planned. While 1&1 expects Vodafone to start to start growing its customer contracts at the same or higher rate, I don’t see a strong catalyst for it given maturing market and the fact that promotional activity has recently been intense (Q4 2025 United Internet Earnings (Notion)).

Modest customer contracts growth: 1&1 expects only modest customer contract growth in 2026 despite losing 70,000 customers last year due to migration and network outage (Q4 2025 United Internet Earnings (Notion)). I would have expected it to return to 100-150k growth again. My gues is that they may be doing this intentionally as it won’t make sense to spend on marketing and end up paying more to Vodafone (as they will grow faster).

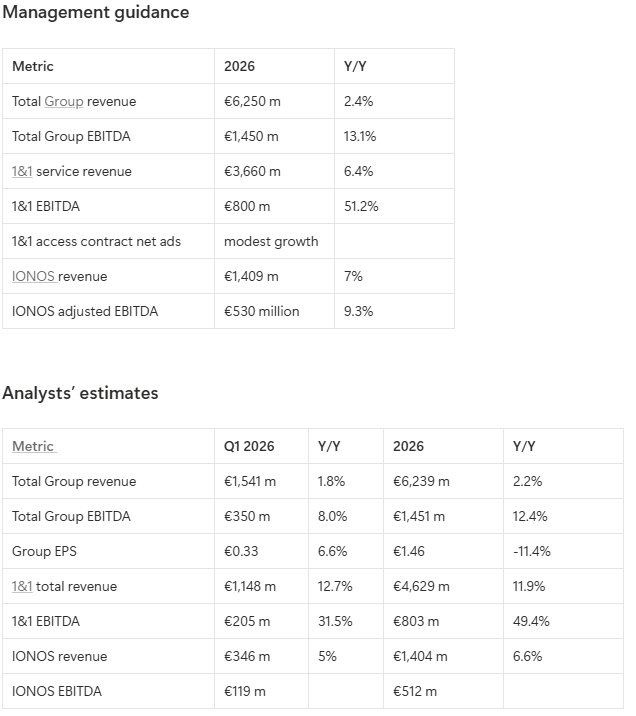

Here are analysts estimates and management guidance for Q1 2026 and FY2026

I=10 United Internet shares up 5% due to stable earnings and solid IONOS performance

United Internet’s Q1 2026 revenue rose 2.5% y/y to €1,552 m, above my estimate of €1,543 m, EBITDA rose 2.4% y/y to €331 m, below my estimate of €344 m while EPS of €0.36 was above my estimate of €0.33.

1&1 Q1 2026 revenue rose 12.5% y/y €1,146 m (my estimate: €1,162 m), EBITDA rose 23% y/y to €192.4 m (my estimate: €198 m) while EPS of €0.10 was in line with my estimate.

1&1 access contracts totaled 16.35 million (-0.18% y/y, flat q/q), driven by improving trends in mobile and broadband contracts, which grew 0.48% and fell 2.3% y/y, respectively.

Management reiterated revenue and EBITDA guidance of 1&1 and United Internet.

1&1’s network continues to add around 200–300 active antenna sites, with coverage currently reaching around 30% of German households (vs. 27% at the end of 2025) and management targeting 35% coverage by year-end (total of 3,000 active sites).

Dommermuth said in the earnings call that getting the low-band spectrum remains uncertain and that BNetzA is proposing that incumbents pay 1&1 €6 m per year for 5 years to compensate for it.

Competition in the mobiled and fixed-line business remains intense but is improving, with management starting to moderately increase prices.

Dommermuth pointed out that data growth rates of 1&1 and Vodafone have begun to converge though that of Vodafone is still lower.

IONOS continues to deliver strong performance, with pricing improving and no signs of AI disrupting the business.

Assessment

United Internet shares are up 5%, probably boosted by solid performance at IONOS. IONOS shares on the other hand are up 8%.

Overall, management’s remarks and answers during the earnings calls lowered some of my worries. For instance, the fact that data growth rates of 1&1 and Vodafone have begun to converge lowers the risk that national roaming costs could come higher than expected again. Additionally, the €6 m per year compensation to 1&1 may be enough to compensate for the costs of securing additional national roaming to cover the 5% traffic gap.