This topic covers Bumble’s Q1 2025 earnings. A preview of the results will be posted here. For the full earnings preview and earnings call summary, see the Notion:

Earnings date: May 5, 2026

Time of Earnings release: 4:00 PM ET

Time of Analysts Call: 4:30 p.m. ET

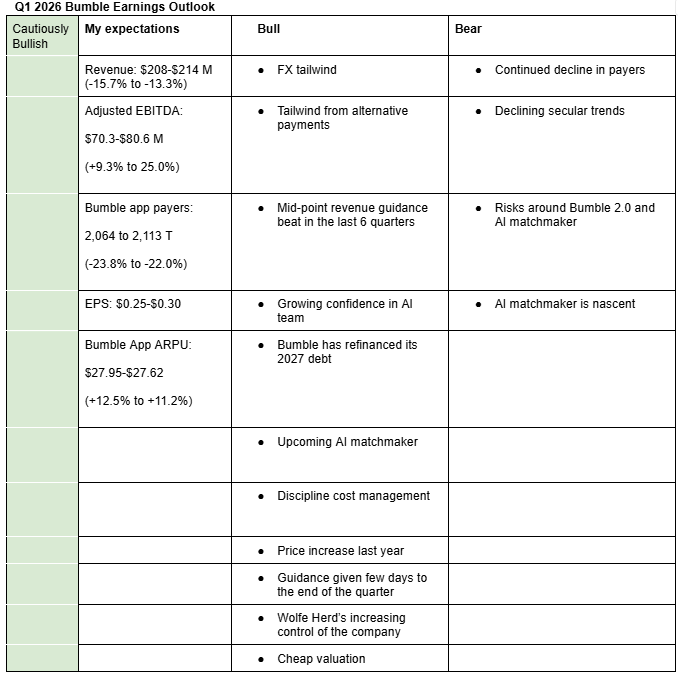

I am cautiously bullish on Bumble’s Q1 2026 earnings and the company overall. My estimates (Bumble Valuation Model (Google Sheets)), takes into account declining payers, price increase last year, management guidance, tailwind from alternative payments, FX tailwind, and discipline cost management. Here is a description of each argument.

Bullish arguments

FX tailwind: During Q1 2026, the USD continued to weaken against major foreign currencies associated with Bumble such as Euro and the Pound. As a result, I expect FX tailwind of around 4.6% and 2% in Q1 2026 and Q2 2026, respectively (Bumble FX Estimates (Google Sheets)).

Tailwind from alternative payments: Bumble said in Q4 2025 earnings call that they saw a full percentage benefit from direct payments in Q4, without any headwind on revenue (Q4 2025 Bumble Earnings). We estimate the cost-savings from the introduction of direct payments is around 1.4% of total revenue in Q1 2026 (Bumble Alternative Payments (Google Sheets)).

Mid-point revenue guidance beat in the last 6 quarters: Bumble has exceeded the mid-point of management’s revenue guidance by an average of 1.8% in the most recent six quarters. Additionally, it has execeeded the mid-point of management’s adjusted EBITDA guidance by an average of 5.3% in the most recent eight quarters: Bumble guidance versus actuals (Google Sheets).

Growing confidence in Bumble’s AI team: Bumble seems successful in attracting strong AI talent, especially from companies such as Amazon and Indeed (Bumble Management (Google Sheets)). Also, the fact that they have already announced a pilot version of the AI Matchmaker makes me believe that they can launch market-ready version on time. That said, insights on the AI Matchmaker from the Q1 2026 earnings will be crucial for the company’s outlook.

Bumble has refinanced its maturing 2027 debt: Bumble announced last week that it has completed refinancing of its $582 million debt which was scheduled to mature in 2027, removing one of the major overhangs on the stock. While the terms of the new debt doesn’t seem fair, it buys them time during the turnaround phase (Bumble debt refinancing (forum)).

Upcoming AI Matchmaker: While the AI Matchmaker is still nascent, there is a strong interest for it from users (Bumble Products and Competition (Notion)). In my opinion, the AI Matchmaker could fix endless swiping, which is one of the major pain points of users.

Discipline cost management: Bumble’s Q4 2025 adjusted EBITDA beat estimates in what the management termed as discipline cost management. In my opinion, the cost-savings from employee layoff in June last year will be felt this quarter. Also, AI is helping Bumble reduce costs by making certain processes (e.g. in product department) more efficient (Q4 2025 Bumble Earnings (Notion)).

Price increase last year: Bumble increased prices last year, starting in Q2 (Bumble Valuation Model (Google Sheets). This tailwind will also be felt in Q1 2026.

Guidance given few days to the end of the quarter: Bumble’s managment guidance was given on March 13. That is only two weeks to the end of the quarter, hence management likely had a strong visibility on the quarter’s performance.

Wolfe Herd’s increasing control of the company: Blackstone, one of the major Bumble shareholders has been significantly selling Bumble shares. As at April 6, 2026, Blackstone’s share of voting rights was 49% versus 65% one year ago. Alternatively, Wolfe Herd’s share of voting rights stood at 35% in April 6, 2026 versus 27% one year ago (Bumble’s Ownership (Google Sheets)). Additionally, it was announced yesterday that Jon Korngold, who was in charge of Blackstone’s investment in Bumble, will leave Blackstone (forum post). This raises the possibility that Blackstone could dispose more of Bumble’s shares. Herd’s increasing control of the company would mean that decisions are beneficial to all shareholders. For instance, we feel that the TRA buyout was not the optimal one (Bumble (Notion)).

Cheap valuation: Despite the 15% gain in share price year-to-date (YTD), Bumble’s valuation is still cheap, trading at around 1x EV/Sales (Bumble (Google Sheets)).

Bearish arguments

Continued decline in payers: Bumble’s payers continue to decline, partly due to secular trends and trust and safety measures introduced last year to improve the quality of the platform. The management expects some sequential improvement in 2026 (having observed stabilizing trends) (Q4 2025 Bumble Earnings (Notion)), but I think real improvements will only arrive once Bumble launches the AI Matchmaker.

Declining secular trends: Dating apps such as Bumble and Tinder continue to lose users due to a combination of swipe fatigue, Gen Z’s need for authenticity and privacy, e.t.c. The trend could continue until better AI match-making features come into force, probably after the second half of 2026: Bumble Market (Notion)

Risks around Bumble 2.0 and AI Matchmaker: There is a risk that Bumble may witness user churn as it transitions to Bumble 2.0. It’s also possible that it might take a while before the AI Matchmaker could be incremental to revenue and payers. In my opinion, even if the rollout of these two products go well, Bumble may have to significantly increase marketing expenses to increase the usage of the AI Matchmaker.

AI Matchmaker is nascent: While the AI Matchmaker holds a lot of promise, it’s still new and how users react and adopt it cannot be predicted with certainty (Bumble (Notion)).

Here are management and analysts estimates for Q1 2026 and Q2 2026:

Q1 2026 management guidance for revenue: $209-$213 million (-15.4% to -13.8%).

Q1 2026 management guidance for adjusted EBITDA: $76-$80 million (+18.0% to 24.2%).

Q1 2026 consensus analysts estimate for revenue: $211.6 million (-14.4%).

Q1 2026 consensus analysts estimate for EPS: $0.28

Q2 2026 analysts estimate for revenue: $215.0 million (-13.4%)

Q2 2026 analysts estimate for EPS: $0.24

Q2 2026 Aron’s estimate for revenue: $214.2 million (-13.7%)

Q2 2026 Aron’s estimate for EPS: $0.25

Q2 2026 Aron’s estimate for Adjusted EBITDA: $57.2 (-39.5%)

I=10 Bumble Q1 2026 revenue in line with estimates, adjusted EBITDA above estimates, but Q2 revenue guidance below expectations

Bumble’s Q4 2025 (press release) revenue fell 14% y/y to $212.3 m, roughly in line with analysts’ estimate and midpoint management guidance $211 m, adjusted EBITDA was $82.6 m, above management upper point guidance of $80 m, while diluted EPS came in at $0.34 versus analysts’ estimate of $0.30.

Bumble app payers fell 23.1% y/y to 2.082 m, rougly in line with my estimate-with the rate of decline improving quarter over quarter, while Bumble app average revenue per payer (ARPU) rose 11.3% y/y to $27.65, also roughly in line with my estimate.

It guides Q2 2026 revenue in the range of $205-213 million (-17.4% to -14.9% y/y), below my base estimate of $214.2 m and adjusted EBITDA in the range of $65-70 million (-31.3% to -26.0% y/y) versus my base estimate of $57.2 m.

In the earnings call, Wolfe Herd said they will launch the new tech stack in the coming weeks and that they are ramping development of the AI matchmaker, which will launch in select markets in Q4 2025 (a bit later than earlier expectations).

Herd added that early testing of the AI matchmaker shows members willing to engage deeply with it and share richer context about preferences.

Herd also said the member base has stabilized, while a separate filing shows Bumble app registrations at around 4 million versus 6 million before the quality reset, monthly active users at around 18 million versus 22 million pre-reset, and U.S. Week 1 retention improving 7% following the reset.

Assessment

Bumble shares were initially up 4% but are now down 3.5%. The market may have disliked the fact that the AI matchmaker (powered by Bee) is coming in Q4 as that signals they are not moving fast enough.

Investors may have also disliked the Q2 revenue guidance as it create uncertainty on the payer numbers. If ARPU growth stays strong at around 11%, the guidance would indicate an accelaration in QoQ payer decline but if ARPU growth was to decelerate to around 3%, the payer numbers would improve sequentially. My guess is that it’s the later given some strengthening in the USD and the fact that price increase began in Q2 2025 (we are lapping strong comps).

Overall, Wolfe Herd remains quite confident that its upcoming AI matchmaker will fix the current secular trends faced by the dating industry. However, the timeline of when it will fix Bumble’s declining payers remains uncertain.