Corporate debt maturities refer to the scheduled dates when U.S. companies must repay the principal on outstanding bonds or loans. These maturities are critical in corporate finance, as firms must either repay the debt using cash flows, refinance it, or default if they lack sufficient funds.

Key characteristics of corporate debt maturities:

Short-term vs. Long-term Debt: Companies issue debt across different maturities, ranging from commercial paper (due in a few months) to corporate bonds (which can extend beyond 30 years).

Refinancing Needs: When large amounts of corporate debt mature in a given year, companies must either refinance at prevailing interest rates or pay off the debt.

Debt Schedules Vary by Sector: Capital-intensive industries (e.g., energy, telecom, real estate) typically have larger refinancing needs due to high debt loads.

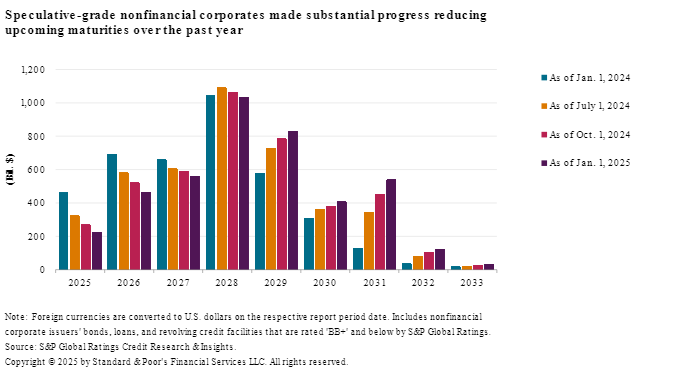

From January 2024 to January 2025, global corporate maturities fell:

2025 maturities dropped by 18%** as companies refinanced or paid down debt.

2026 maturities declined by 5.6%.

Speculative-grade debt maturities fell by 51% for 2025, as companies refinanced ahead of upcoming obligations.

In 2025, speculative-grade maturities make up just 12% of the total. By 2028, this percentage rises to 40%, totaling $1.11 trillion in speculative-grade debt.

U.S. and European ‘BBB’ bonds refinancing in 2025-2026 will see an increase of 170-195 basis points.

Assessment: The surge in debt issuance in 2024 facilitated the refinancing of existing obligations but did not completely alleviate the overall debt burden, with total maturities still exceeding $2 trillion in all tears. In my view, favorable liquidity conditions in 2024 played a key role in keeping refinancing markets open and supportive. However, with liquidity growth now seeming to be decelerating, 2025 could present a more challenging environment for refinancing.