FED Net Liquidity: FED balance sheet -TGA - Reverse Repo

FAQ

What is Fed Net Liquidity?

Fed Net Liquidity is a measure of the amount of money available in the financial system that can be used for lending, investments, and financial market activity. It is often approximated using the following formula:

Fed Net Liquidity=Fed Balance Sheet−(Reverse Repo+Treasury General Account)

Where:

• Fed Balance Sheet (Reserves): The total assets held by the Fed, including Treasuries and Mortgage-Backed Securities (MBS).

• Reverse Repo (RRP): Money that financial institutions have parked at the Fed, effectively removing it from circulation.

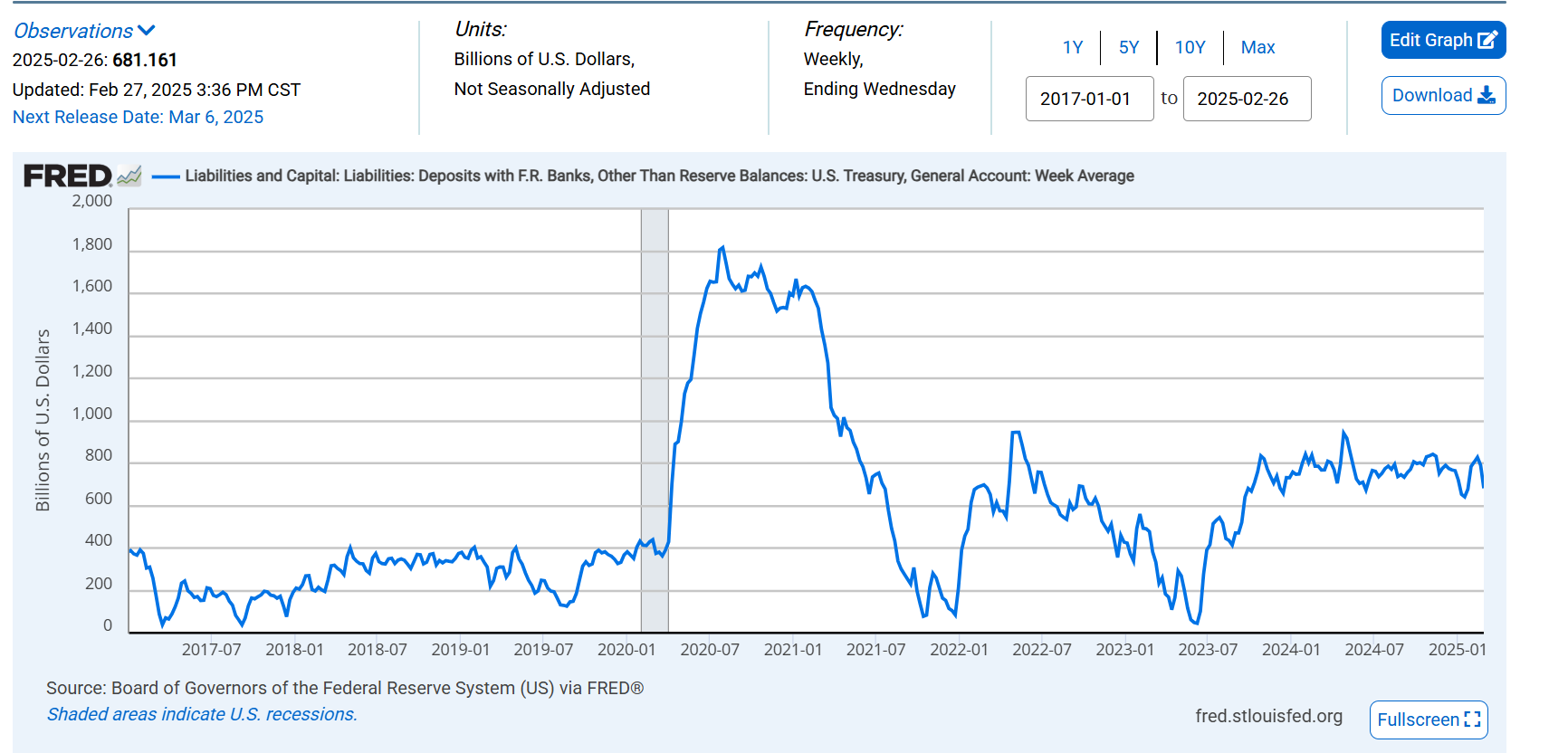

• Treasury General Account (TGA): The U.S. government’s cash balance at the Fed. A rising TGA means the government is sucking liquidity from the system, while a falling TGA adds liquidity.

Why is RRP Depletion Good for Fed Net Liquidity?

1. Less Money is Locked at the Fed → More Cash in the System

• When institutions withdraw from the Reverse Repo facility, the cash returns to the banking system rather than sitting at the Fed.

• This increases bank reserves, making it easier for financial institutions to lend and invest.

2. Direct Impact on the Net Liquidity Formula

• Since Fed Net Liquidity is inversely related to RRP, a decline in RRP mathematically increases net liquidity.

3. Improves Market Functioning

• Higher liquidity lowers short-term funding stress, improves market stability, and supports asset prices.

4. Counteracts Quantitative Tightening (QT)

• The Fed is reducing its balance sheet (QT), which normally tightens financial conditions.

• However, RRP depletion offsets some of that tightening by replenishing bank reserves.

Final Takeaway

Fed Net Liquidity rises when RRP falls because cash that was previously parked at the Fed re-enters the financial system, increasing bank reserves and supporting lending, investments, and asset markets.

Why is the Treasury General Account (TGA) Negative for Fed Net Liquidity?

The Treasury General Account (TGA) is the U.S. government’s cash balance held at the Federal Reserve. When the TGA balance increases, it means the government is pulling money out of the financial system, reducing the amount of liquidity available to banks and markets. This is why TGA is subtracted in the Fed Net Liquidity formula:

Fed Net Liquidity=Fed Balance Sheet−(Reverse Repo+TGA)\text{Fed Net Liquidity} = \text{Fed Balance Sheet} - (\text{Reverse Repo} + \text{TGA})Fed Net Liquidity=Fed Balance Sheet−(Reverse Repo+TGA)

How the TGA Works & Its Impact on Liquidity

- Government Borrowing (TGA Increases → Liquidity Decreases)

- When the Treasury issues bonds (U.S. government debt), investors buy them, and the proceeds go into the TGA at the Fed.

- This removes cash from the banking system because money that was circulating now sits idle in the TGA.

- Result: Fed net liquidity drops.

- Government Spending (TGA Decreases → Liquidity Increases)

- When the Treasury spends money (e.g., paying government salaries, infrastructure projects, or Social Security), the money flows out of the TGA and into bank accounts.

- This adds liquidity back into the financial system.

- Result: Fed net liquidity rises.

Example of TGA’s Impact

- Suppose the TGA increases from $300 billion to $800 billion due to new Treasury bond sales.

- That extra $500 billion is effectively removed from bank reserves and financial markets, tightening liquidity.

- Conversely, if the Treasury spends down the TGA (e.g., dropping it from $800B to $300B), that $500 billion flows back into the economy, increasing Fed Net Liquidity.

Why TGA Matters for Markets

- If TGA is rising, liquidity is being drained, which can tighten financial conditions and hurt asset prices.

- If TGA is falling, liquidity is increasing, which can ease market stress and support risk assets like stocks and bonds.

Final Takeaway

The TGA is negative for Fed Net Liquidity because money held in the Treasury’s account at the Fed is not circulating in the banking system. When the government increases its TGA balance (by issuing more debt than it spends), it pulls liquidity out of markets. When the Treasury spends down its TGA, it injects liquidity back into the system.