Main Article: Euro Zone Inflation - InvestmentWiki

Eurozone headline inflation continues to decline, while core prices remain very sticky, do not show signs of easing on a y/y basis, and services contribution continues to increase. The only positive sign I see is a -0.1m/m for core prices, which if it continues will eventually bring down the y/y rate.

With these numbers, IMO another hike is given. And would not discard more yet, seems Lagarde always sounds very hawkish, however, the economy is weaker, so they probably need to be more balance in policy than the US.

The CPI index in the eurozone seems more balance too, housing rents does not make the huge contribution we see in the US index. But this means any contribution coming from housing will be more limited too.

- The euro area’s annual inflation rate was 5.3% in July 2023, down from 5.5% in June. A year earlier, the rate was 8.9%

- Core consumer prices, stripping out volatile elements like food and energy, rose 5.5% from a year earlier. A year earlier, the rate was 4%

- In July, the highest contribution to the annual euro area inflation rate came from services (+2.47 percentage points, pp), followed by food, alcohol & tobacco (+2.20 pp), non-energy industrial goods (+1.26 pp) and energy (-0.62 pp).

2 Likes

SI=0%, I=7

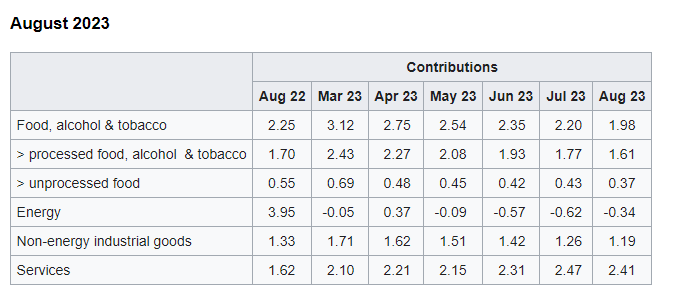

- Preliminary data from the European Statistics office indicate that euro zone headline inflation was 5.3% for August, unchanged from July’s number and above analysts estimate of 5.1%.

- Core inflation moved down to 5.3% from 5.5% in July.

- At 9.8%, food, alcohol & tobacco were the biggest contributor of headline inflation, having moved down from 10.8% in July.

- Services inflation declined to 5.5% from 5.6% in July.

https://ec.europa.eu/eurostat/documents/2995521/17396139/2-31082023-AP-EN.pdf/06f6eed0-f52a-81cc-16e3-30aaf64d81b8

https://www.cnbc.com/2023/08/31/inflation-euro-zone-august-2023.html#:~:text=Inflation%20in%20the%20euro%20zone,the%20European%20statistics%20office%20Thursday.

1 Like

1 Like

August Inflation was revised down to 5.2% y/y, and 0.5% m/m

- The euro area annual inflation rate was 5.2% in August 2023, down from 5.3% in July. A year earlier, the rate was 9.1%.

- European Union annual inflation was 5.9% in August 2023, down from 6.1% in July. A year earlier, the rate was 10.1%.

https://ec.europa.eu/eurostat/documents/2995521/17524083/2-19092023-AP-EN.pdf/7b701ff5-0011-ccc9-8cde-9f559f345ce9

1 Like

SI=2%, I=8

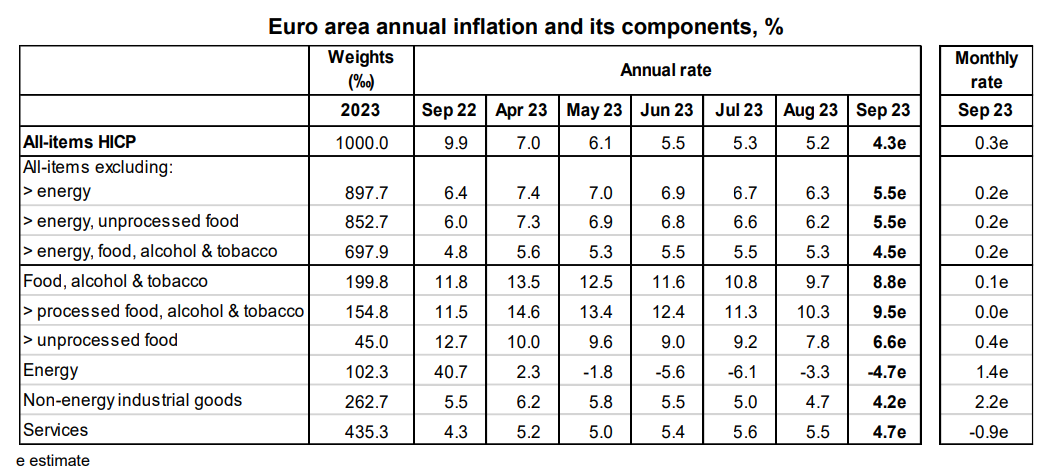

- Eurostat expects Euro zone core inflation to be 4.5% in September, down from 5.3% in August and below Bloomberg estimate of 4.8%.

- Headline inflation is expected to be 4.3% in September, down from 5.2%(revised down from 5.3%) in August and also below expectations.

- The decline in headline inflation was mainly due to a sharp decline in energy costs(-4.7% vs. -3.3% in August) and a drop in services from 5.5% in August to 4.7%.

1 Like

I=7

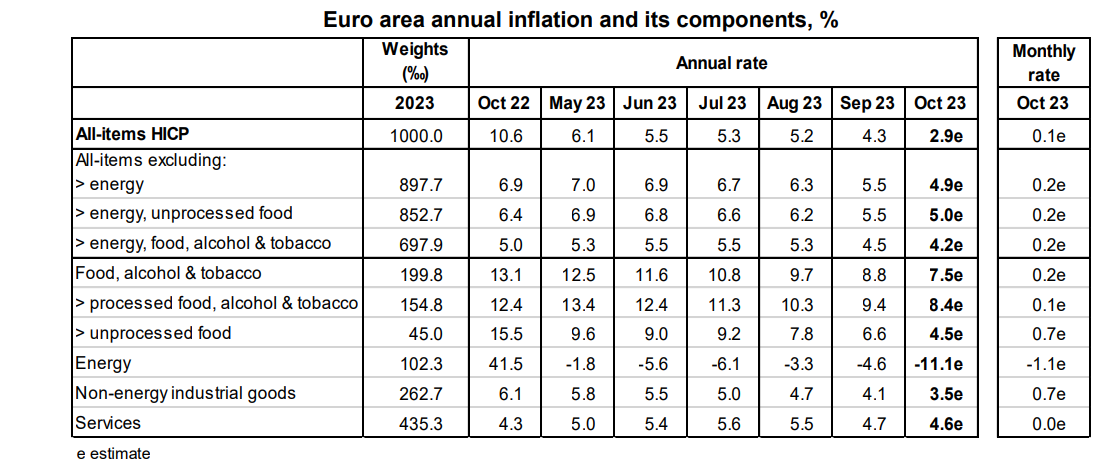

- Eurostat expects Euro Zone inflation to be 2.9% in October, down from 4.3% in September and below 3.1% estimate.

- Core inflation drops to 4.2% y/y, down from 4.5% in September.

1 Like

I=7

- Eurostat expects euro zone inflation to decline to 2.4% in November from 2.9% the previous month, below 2.7% estimate.

- Core inflation eased to 3.6% from 4.2% in October, below 3.9% estimate.

Since Europe is kind of or close to entering a recession, I would not be surprised if inflation falls to 2% or below it sooner than expected, and the EBC has to cut sooner too. This is if the economic weakness continues.

The questions will remain if after the economic recovery inflation will come back up, or if it will stay around target.

2 Likes

I=6

- Eurostat expects Euro area inflation to be 2.9% in December, up from 2.4% in November but in-line with the Bloomberg estimate, mostly due to end of some government subsidies and low energy prices being removed from base figures.

- Core inflation fell to 3.4% from 3.6%.

- Services inflation jumped 0.7% on the month (versus a decline of 0.9% in November) but annual reading was steady at 4.0%.

1 Like

I=6

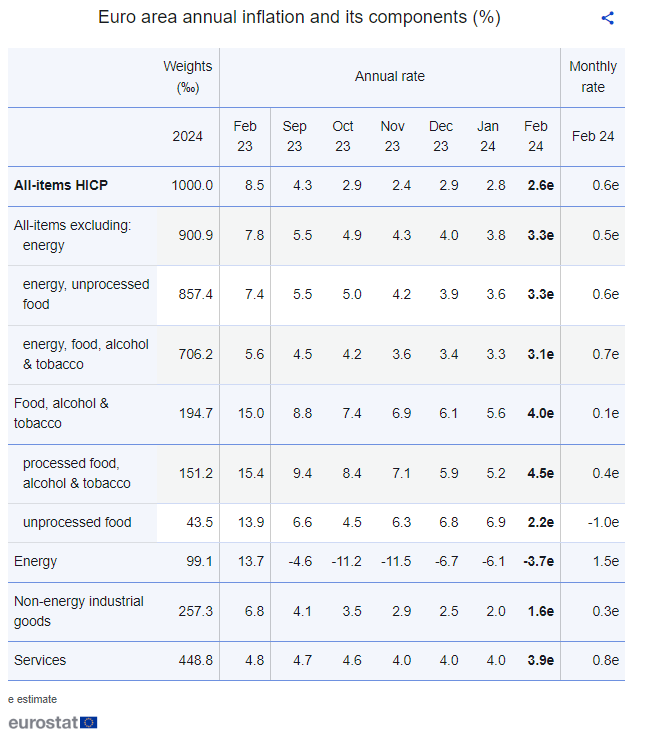

- Eurostat expects Euro area inflation to be 2.6% in February, down from 2.8% in January but above 2.5% estimate.

- Core inflation is expected to be 3.1%, down from 3.3% in January but above 2.9% estamate.

1 Like

I=6

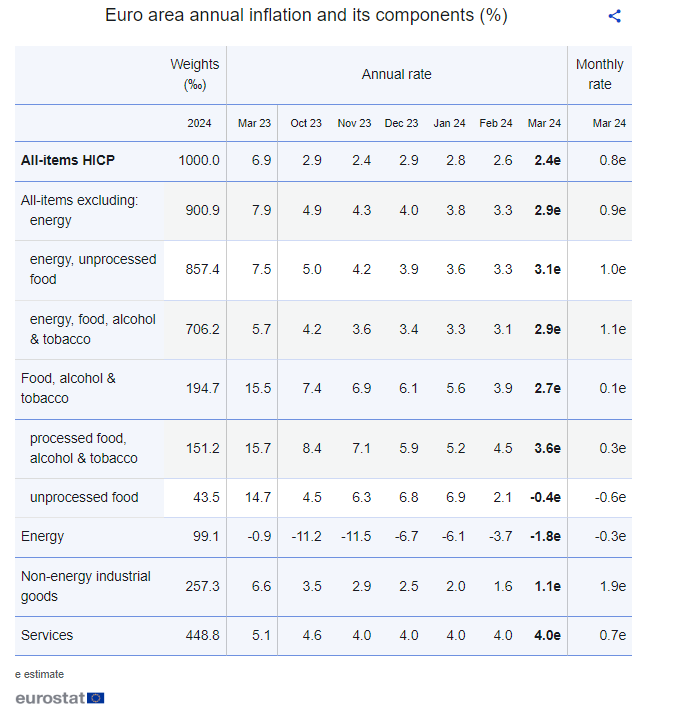

- Eurostat expects Euro zone inflation to slow to 2.4% in March from 2.6% in February, lower-than 2.6% estimate.

- Core inflation is expected to cool from 3.1% to 2.9%, also below expectations.

- Service inflation remained stuck at 4% for a fifth straight month.

2 Likes

Very different scenario for Europe.

But to be fair, their economy is weaker, and a weak economy usually comes with falling inflation.

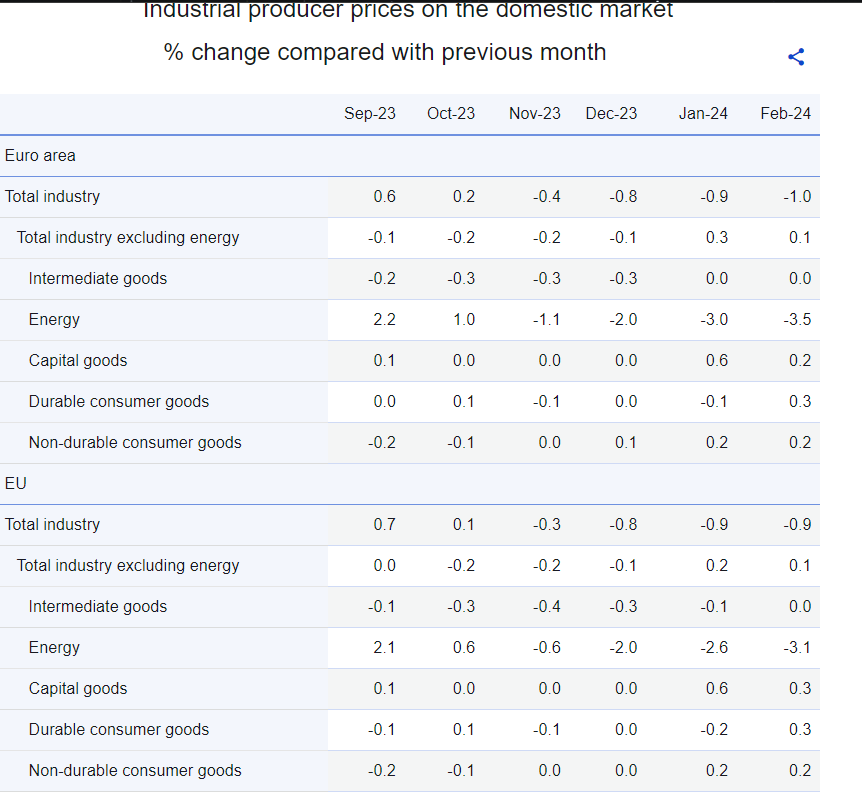

Today PPI also came very soft, but mostly because of energy.

- On a monthly basis, producer prices declined by 1.0%, surpassing market expectations of a 0.7% decrease.

- Decreased by 8.3% year-on-year in February 2024, following a revised 8.0% drop recorded in the preceding month, compared with market expectations of an 8.6% decline.

Industrial producer prices down by 1.0% in the euro area and by 0.9% in the EU - Eurostat

1 Like

I=6

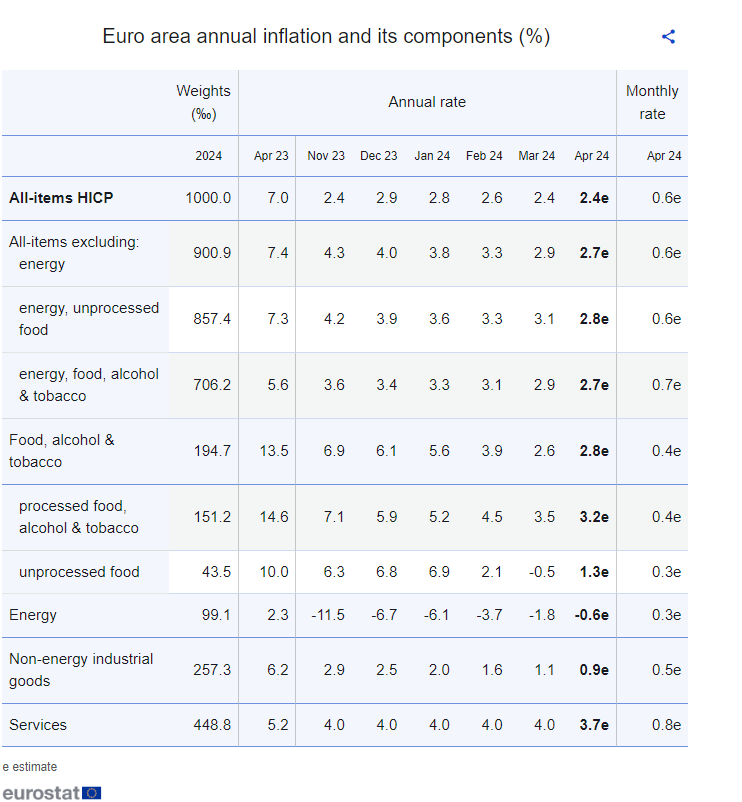

- Eurostat expects Euro zone headline inflation to hold steady at 2.4% in April, in-line with the estimate.

- Core inflation dropped to 2.7% from 2.9% in March, slightly above 2.6% estimate.

- Service inflation dropped to 3.7% after sticking at 4% for five consecutive quarters.

1 Like

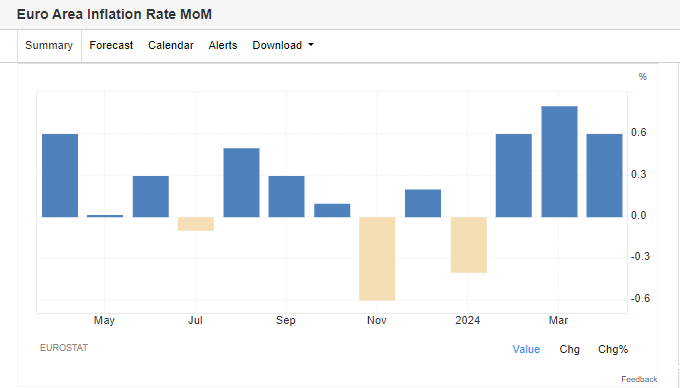

Those monthly increases are high. They have been coming in high in the last 3 months.

Lets hope is not something more, because it seems is common to see higher monthly increases at the start of the year.

1 Like

I=6

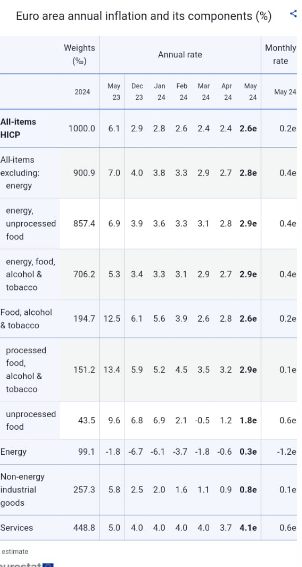

- Eurostat expects Euro zone inflation to rise to 2.6% in May from 2.4% in April but lower than 2.5% estimate.

- Core inflation increased to 2.9% from 2.7% in April against expectations for a flat reading.

- Services inflation rose to 4.1% from 3.7% in April.

- Fluctuations in the ECB reading were projected over the coming months due to base effects from the energy market and end of government subsidies.

- The market is still pricing in a rate cut in June and a one more rate reduction in 2024 despite the increase in inflation reading this month.

2 Likes

I=6

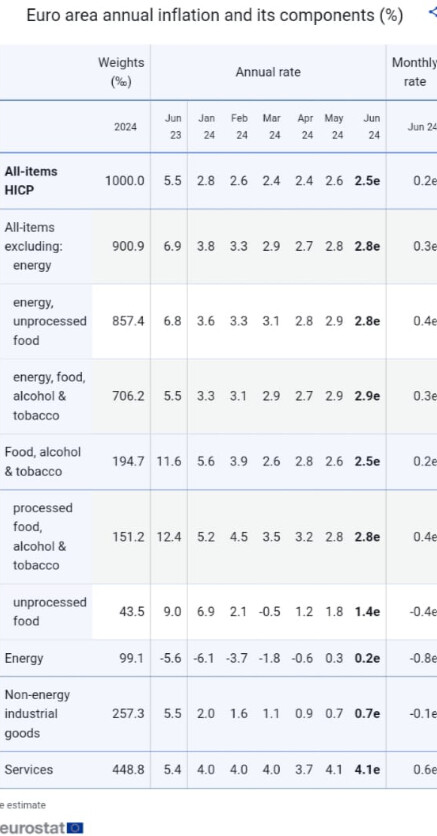

Euro zone headline inflation eases to 2.5%, core misses estimate

- Headline inflation in the euro zone fell to 2.5% in June from 2.6% in May, in-line with the estimates.

- Core inflation remain steady at 2.9%, above 2.8% estimate.

- Services inflation was also steady at 4.1% while energy prices were up 0.2%.

2 Likes

I=6

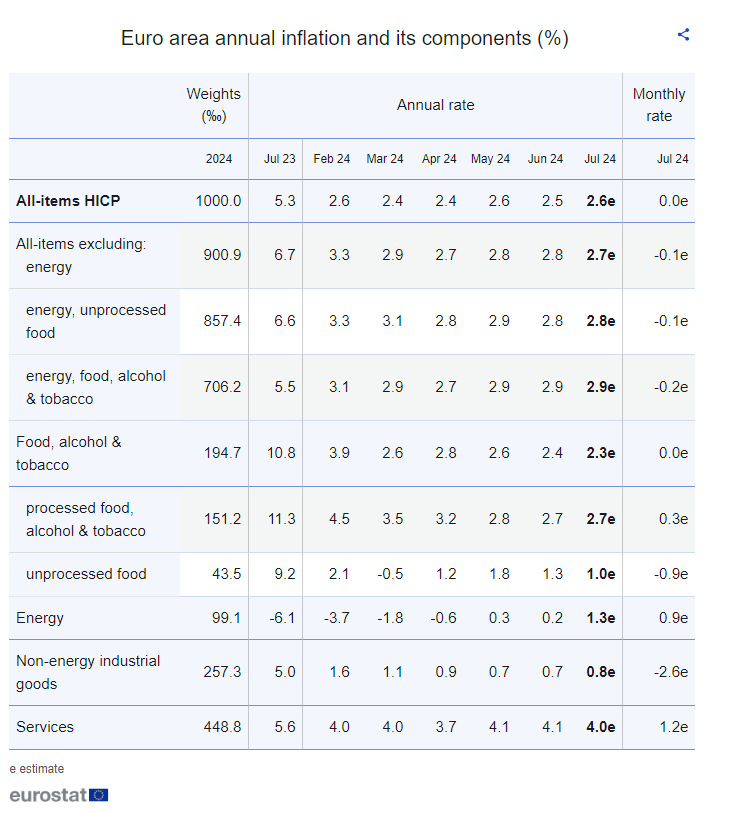

Euro zone inflation rose to 2.6% in July, against expectations

- Headline inflation rose to 2.6% in July, against expectations for it to stay steady at 2.5%.

- Core inflation was steady at 2.9%, above 2.8% estimate.

- The closely watched services index fell to 4% from 4.1% in June.

1 Like

I=6

Euro zone inflation fell to 2.2% in July, in line with expectations

-

Euro zone inflation fell to 2.2% in August from 2.6% in July, in line with the estimates.

-

Core inflation declined to 2.8% from 2.9% in July, also in line with expectations.

1 Like

I=6

Euro zone inflation fell to 1.8% in September, in line with expectations

- Euro area inflation fell to 1.8% in September from 2.2% in August, in line with estimates.

- Core inflation fell to 2.7% versus expectations for it to stay steady at 2.8%.

1 Like