This topics aim is to understand, project and discuss dollar liquidity reserves in the next years taking into account effects of quantitative tightening (QT), new debt issuances, actions of foreigns governments, usage of the treasury general account and more.

Quantitative Tightening:

Quantitative tightening programs are design to reduce the FEDs balance sheet by 95 billion per month but are tracking behind. From April 2022 until 2023 the FED balance sheet dropped from 8,965 billion to 8,500 billion or 5.19%.

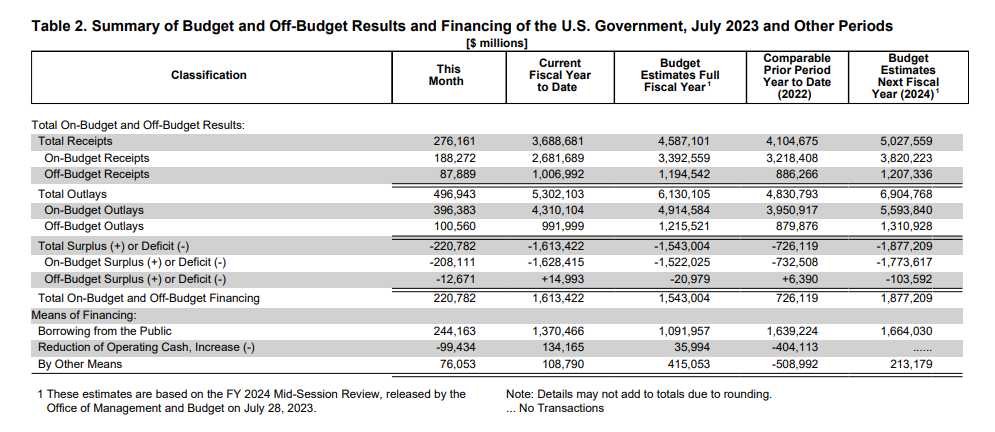

New debt issuance: U.S. debt exploded during covid from 23.500 billion to over 30,000 billion. New debt issuance for 2023 and 2024 are projected to be: …

Treasury General Account:

Note @magaly: This post is a Wiki post and can be edited from multiple team members who have the permission to edit. The goal is to provide a very brief overview over the topic, our research and why it is important. My first post here is just a quick draft and example of the direction i am thinking of. Summaries of different topics in the initial post should be ultra short and invite people to explore more in the Wiki.

@magalymight be helpful for your research. High net worth individuals have higher cash equivalent allocations than usual at 34% of their portfolio up from 24% a year ago and family offices are looking to increase the % of fixed income from 12 to 15% according to a study of Capgemini.

We will have to find out if the amounts are significant. Also if they are using bank funds to buy treasuries, it will still be negative for bank reserves.

Ray Dalio warning that the debt path of the US will lead to an imbalance of supply and demand. We are at the brink to found out if there are enough buyers to sustain all the debt in the next 1 to 2 years.

Very interesting. In case there are not enough buyers i guess interest rates would rise and money come from other (debt) sectors like mbs, corporate debt etc. correct? (Or even other assets like equities)

Do we have an overview over the debt landscape that tells us how much debt is in which sector?

That could be the case, yes, but that would mean that they would just move the issue from the government to the private sector since they would be sucking their liquidity.

The FED can always do QE too, which I think could be the most likely outcome, and the issue with inflation could be never-ending.

They could choose to inflate the debt away, it has happened before in US and other countries

I don’t think we have that overview, I will work on it.

I think it will. Dollar alternatives are probably going to do very well in this environment, along with equity. But he also says we will experience a financial crisis of some sort, probably a lot of pain before the great returns.

@moritz This is a very interesting interview, but a bit long

He measures the global liquidity cycle in markets and is showing chart/data that liquidity bottomed already at the end 2022. He was right in predicting the last rally since he is saying this since the start of the year.

His argument is similar to the ones we are starting to hear more and more from economists. The amount of debt refinancing needs and government huge deficits will force the FED to do much more QE. This will support asset prices from now on, and be very negative for bonds/cash.

The own CBO projections the FED holding of treasuries will be 7.5 T, from 5 T now. He says this will be even higher. (1:18:00). But apparently, this is not only a FED problem, is more global.

“QE is coming back big time. Central banks have spent much of the last few months bailing out banks. What they’re gonna spend much of the next few years bailing out is governments.”

Larry Fink of Blackrock mentions 7 trillion in money market funds that might go back into equities or bonds at one point. He seems very optimistic about the economy mainly due to persistently high innovation in the U.S.

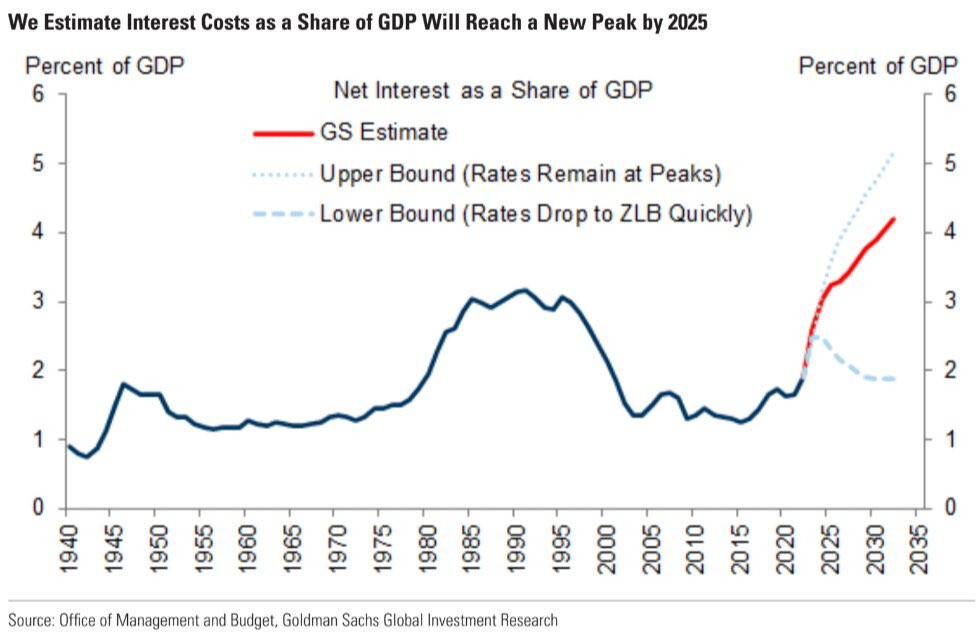

US debt was downgraded from Fitch, something similar happened in 2011 debt ceiling issue. We could see borrowing cost rise even more due to this.

Now S&P and Fitch have down downgraded the US, and probably cant be assessed as a AAA country anymore. But I think markets will continue to see it that way, at least now.

Fitch Ratings downgraded the U.S.’s long-term foreign currency issuer default rating to AA+ from AAA, pointing to “expected fiscal deterioration over the next three years,” as well as a growing general debt burden.

While tax receipts are decreasing very significantly, government spending continues to increase at the same pace.

For FY2023 deficit is already larger than FY2022 by almost 300 billion, with 2 months left still.

This is so unsustainable, to have these fiscal deficit numbers in a year there is even no recession still, with unemployment at decade lows.

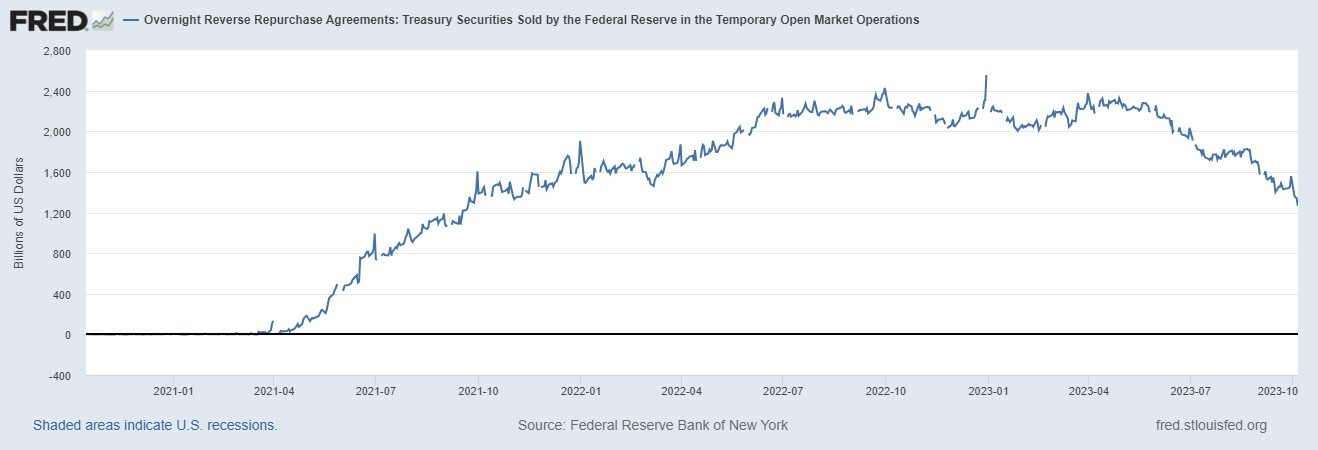

The reverse repo facility was drained by almost 1 trillion in a manner of 3 months after the debt ceiling was resolved.

There is now only approx 1.2T available. When it is completely depleted, is likely the private sector will have to offer or compensate for the liquidity needed to finance the government as long as QT continue.

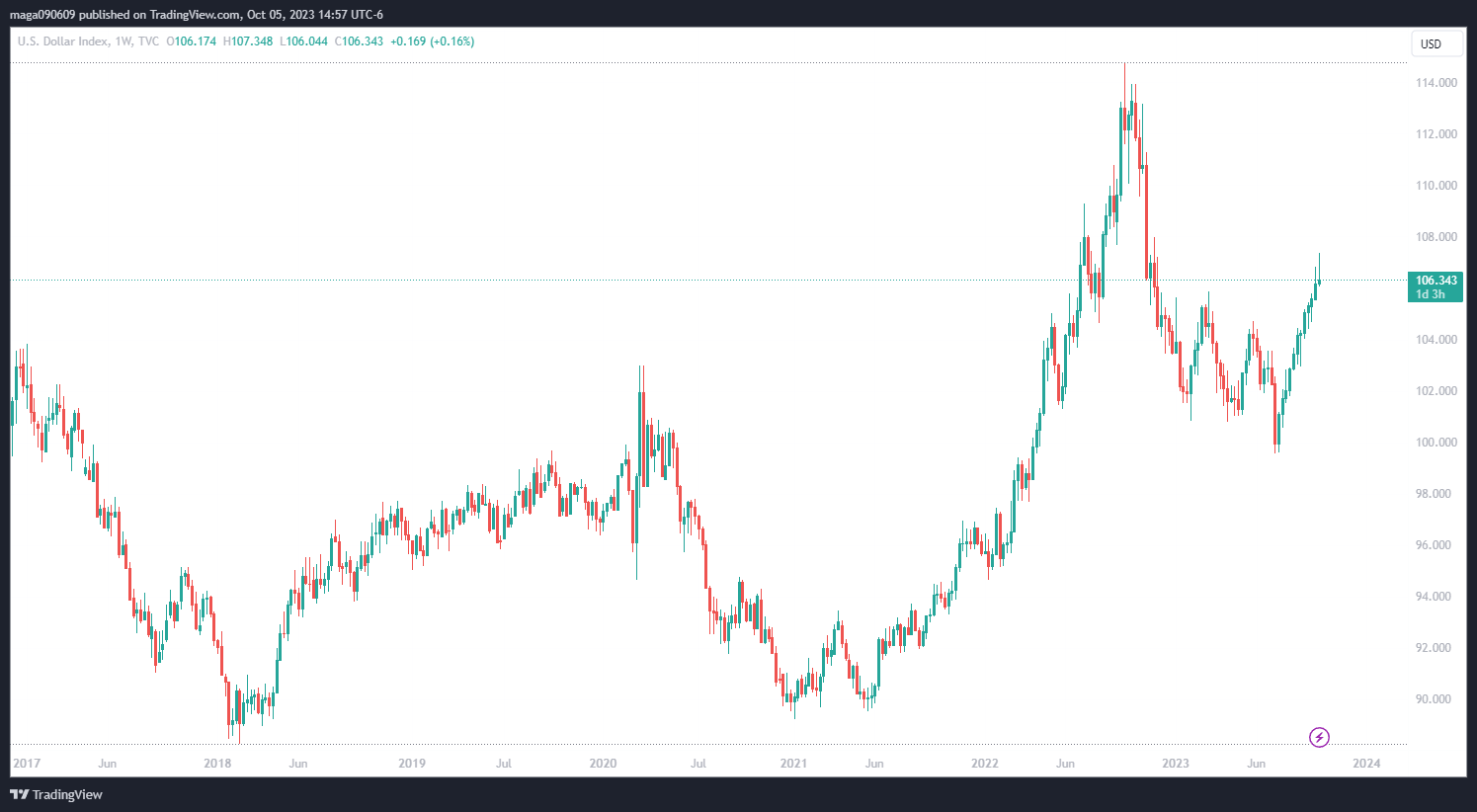

The dollar index has also had a significant run since July, approximately 7% increase.

Every time the dollar gets strong is a significant headwind for liquidity for the rest of the world (we were able to see this in 2022) due to the huge amount of dollars needed for all types of transactions/debt around the world.

If it continues in its path higher, I expect to continue to put constraints on liquidity.

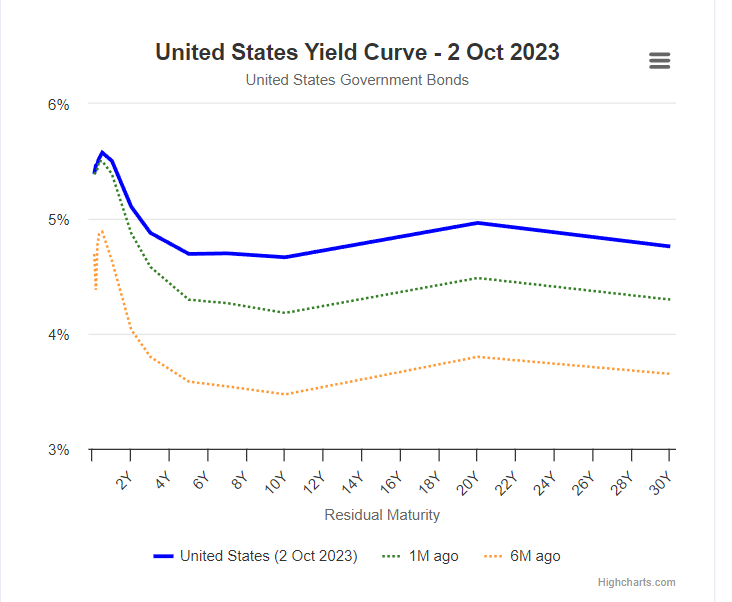

The treasury issued some 20B of 30 years bond, and apparently, the auction did not go too well, even with the amount seemingly low.

The 30-year bond ended up spiking more than 15bps after the auction, and it continued to go up.

High yield at the auction was 4.837%, as reference last auction was 4.125%

Apparent signs that demand at lower yields is not there currently, concerning due to the huge supply expected to come to the markets, and the treasury expected to have to issue more long bonds going forward too.

The reversal in the markets was due to this.

| Michael Howell")