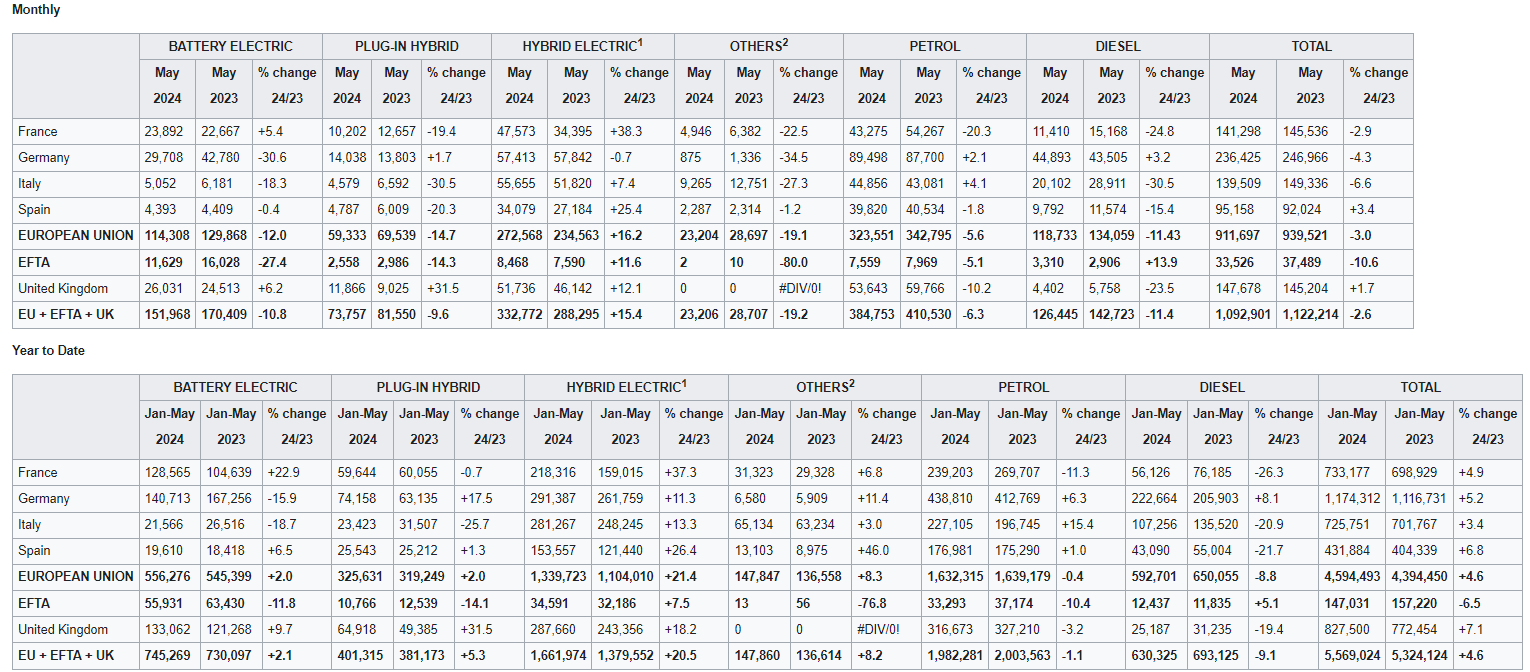

In May 2024, car registrations in the European Union decreased by 3%, with declines observed in three out of the region’s four major markets: Italy (-6.6%), Germany (-4.3%), and France (-2.9%). Spain, on the other hand, achieved a modest growth of 3.4% last month.

In May all growth is due to hybrid electric cars, since all other categories experienced a decline.

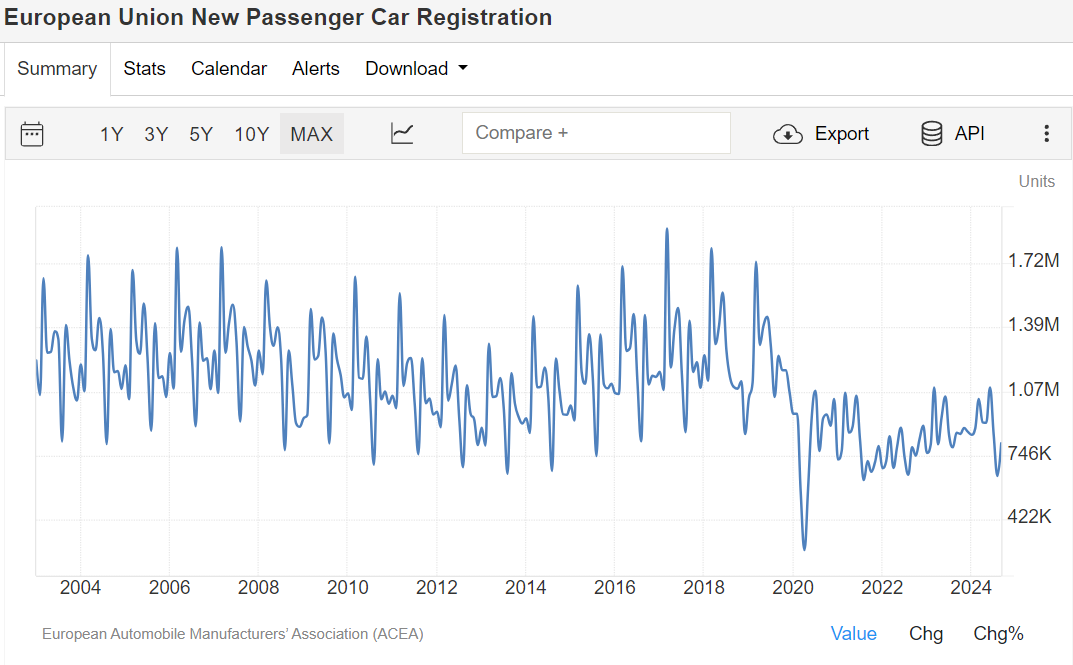

Despite the downturn in May, year-to-date car registrations over the first five months of 2024 increased by 4.6% to 4.6 million units.

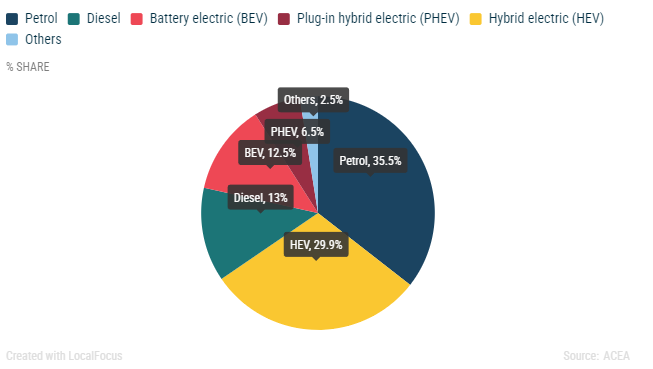

In the first half of 2024, new car registrations increased by 4.5%, reaching nearly 5.7 million units. However, registration volumes remain relatively low (-18%) compared to pre-pandemic levels.

1H2024 growth of 4.5% is higher than the 2.5% growth forecasted by ACEA for 2024. Most of this growth however is due to the hybrid electric car segment.

Last year 2H had lower growth than 1H, so maybe we could expect a bit lower growth rate for 2024 (3-4%).

However, I would like to analyze the whole series at some point to see the seasonal patterns more clearly since last year is not the best comp imo.

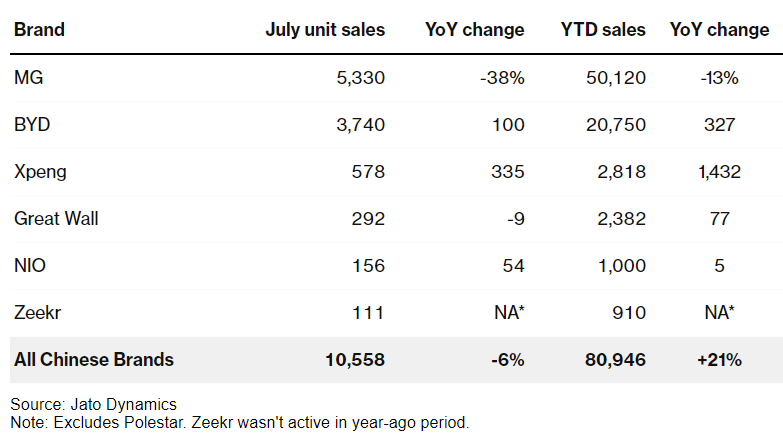

China automakers EV registrations in the EU fell in July, exaggerated by EU tariffs but BYD’s strength holds up

According to data compiled by Dataforce, new EV registrations by Chinese automakers fell by 45% in July compared to June but that may have been contributed by the rush to deliver to dealers in June before the EU tariffs kick in.

However, July figures provided little to suggest that Chinese automakers are slowing down their push to the EU market. For instance, their market share in Europe stood at 8.5% in July up from 7.4% a year ago.

BYD looks particularly immune to tariffs having sold three times more EVs in July compared to a year ago while its pricing strategy was unchanged.

Dataforce figures come from 16 countries that have reported vehicle registration numbers for the month of July.

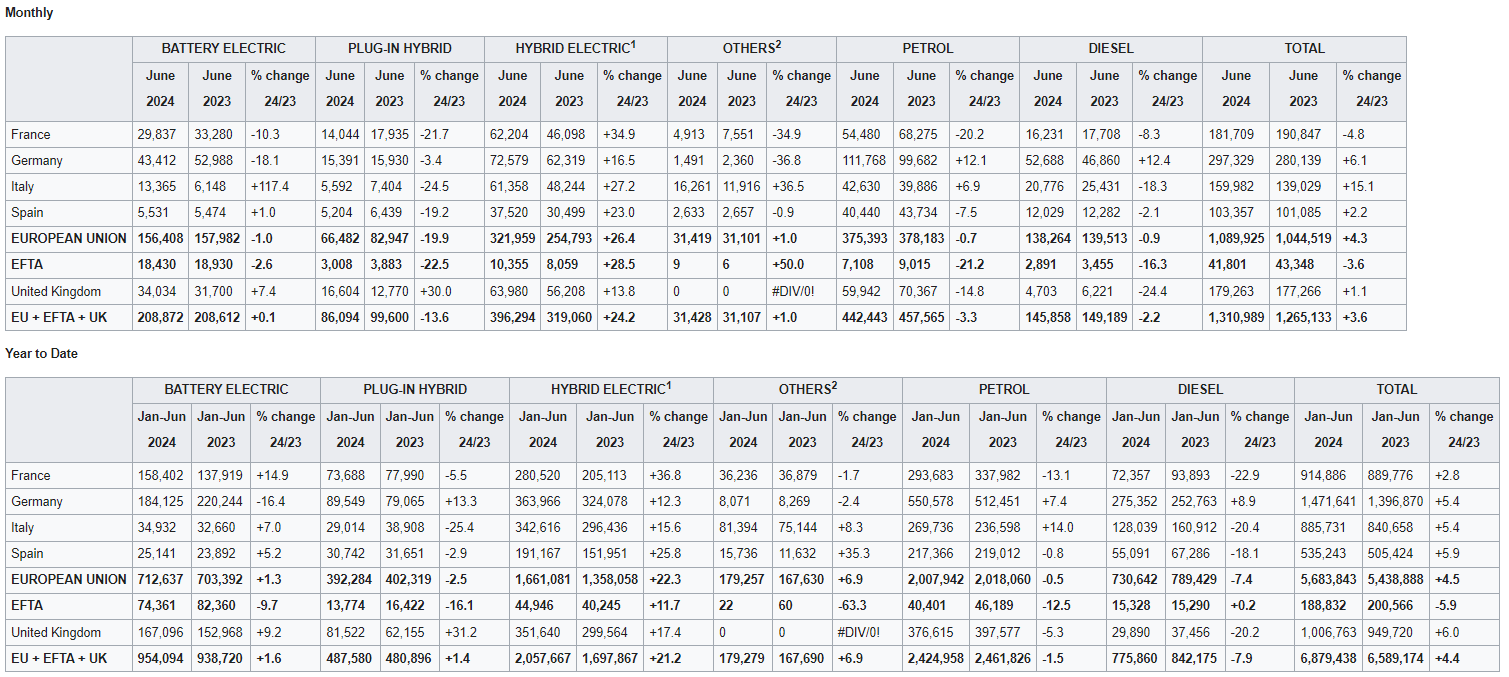

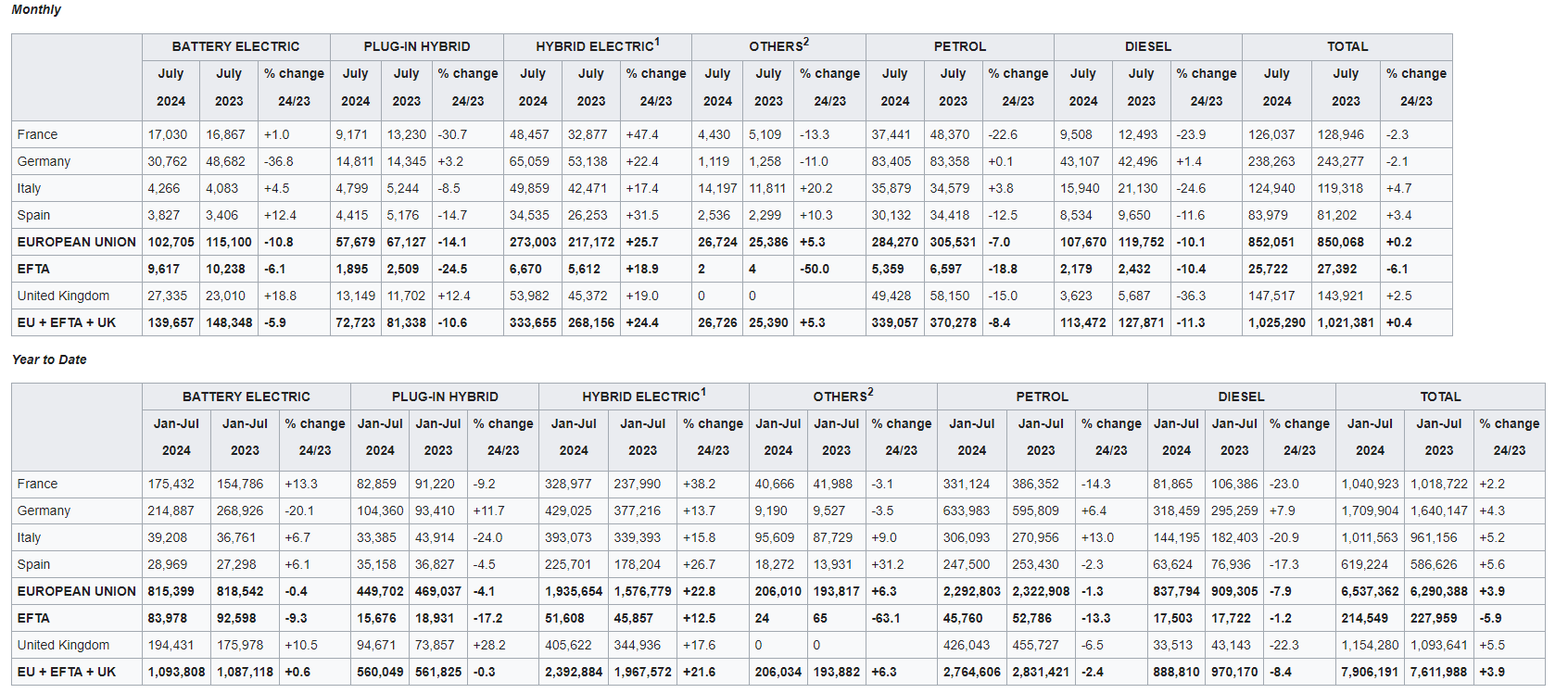

July 2024 Europe Car registrations saw a very modest increase of +0.2% Y/Y

Seven months into 2024, new car registrations increased by 3.9%, reaching more than 6.5 million units. This is the result of a low comparison base.

The bloc’s largest markets all showed positive but modest performance, with Spain (+5.6%), Italy (+5.2%), Germany (+4.3%), and France (+2.2%) all recording growth.

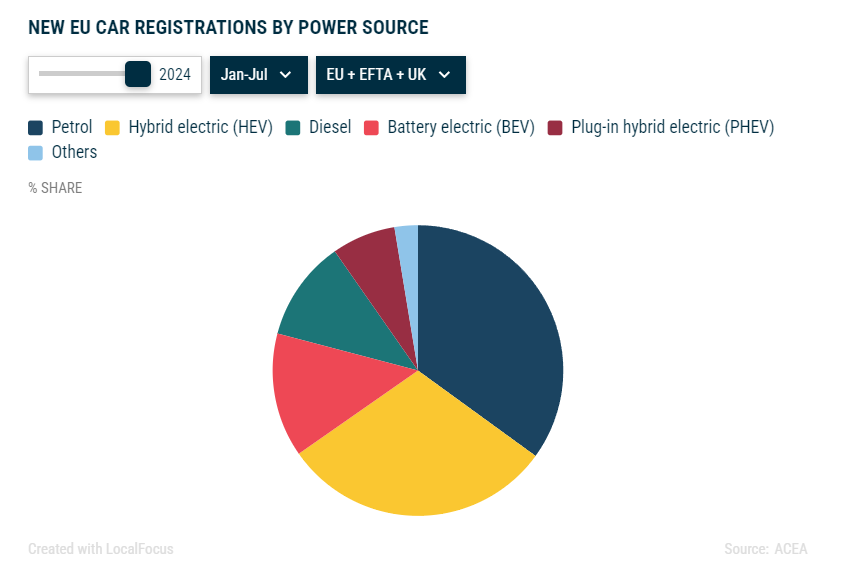

Hybrid Electric continues gaining market share this year, 30.3% vs 25.8% in 2023, and is the only significant segment year to date recording positive growth.

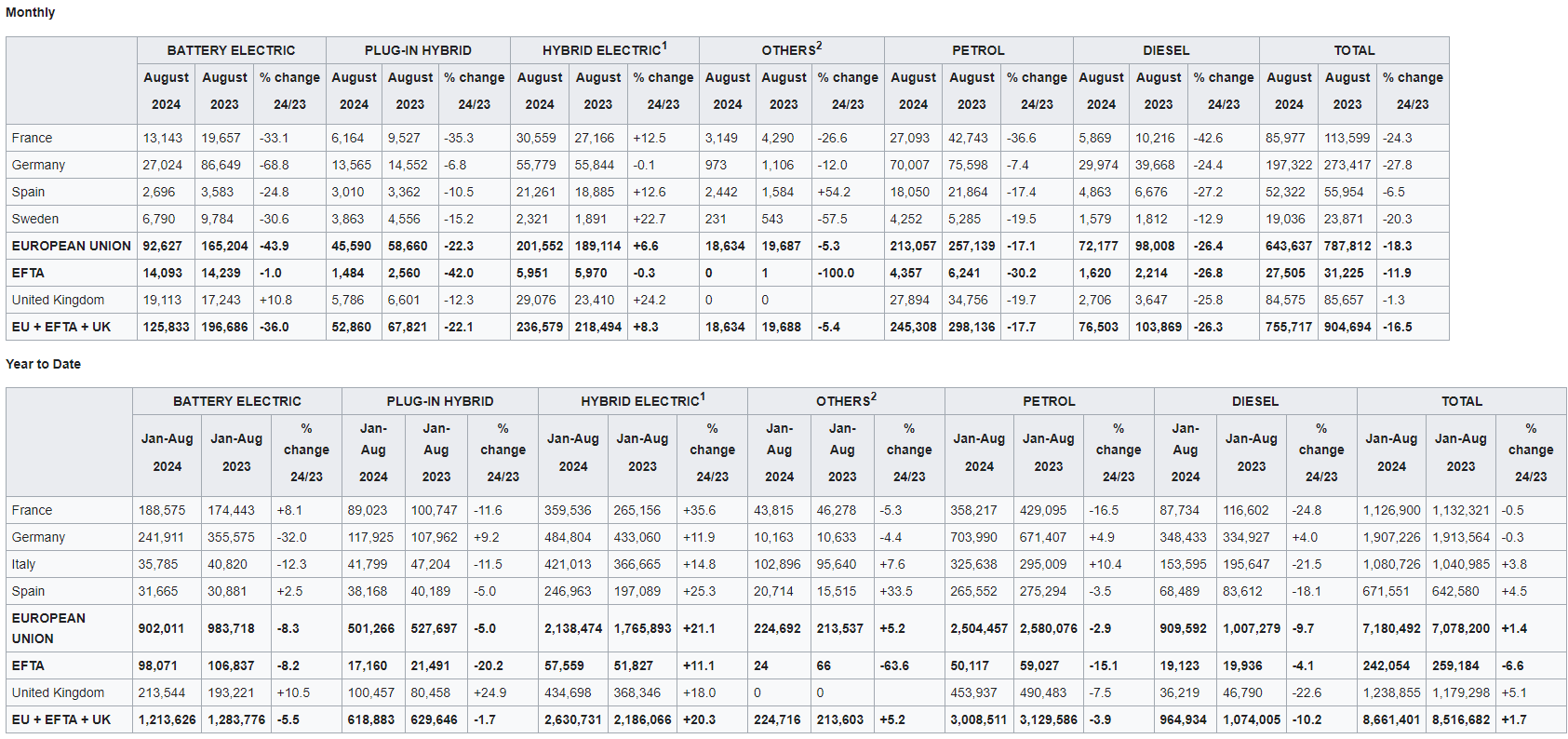

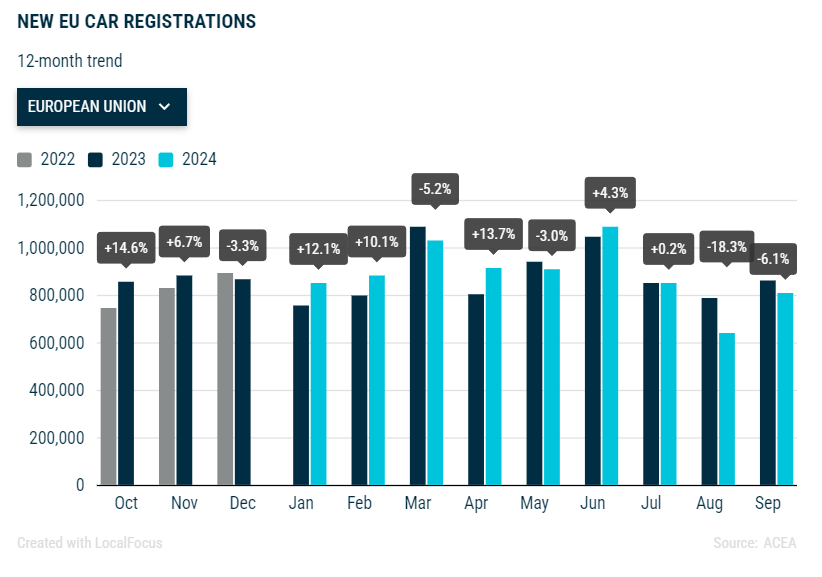

In August 2024, new EU car registrations saw a sharp decrease (-18.3%)

Consumers in core markets of Germany, France, Italy and Spain drove an 18% on-year drop in the bloc’s monthly registrations, which reflect sales, the European Automobile Manufacturers’ Association said Thursday. EU registrations came to around 643,600 for the month, with every major European carmaker posting declines.

Eight months into 2024 , new car registrations increased by 1.4%, almost reaching 7.2 million units.

In August , battery-electric cars accounted for 14.4% of the EU car market, down from 21% the previous year. This represents the fourth consecutive month of decline this year, contrasting sharply with the almost consistent month-on-month increases last year.

Seems there is seasonality in the series, and August is historically a bad month. Last year was not as pronounced probably since demand was catching up.

So, for now I don’t expect this to mean much, but worth to monitor the coming months.

@Magaly i think we need to develop a basic automotive demand model soon. At the current stage we have all this detailed monthly data but I think it’s not easy to see the big full picture of what is happening or what we expect to happen in the future.

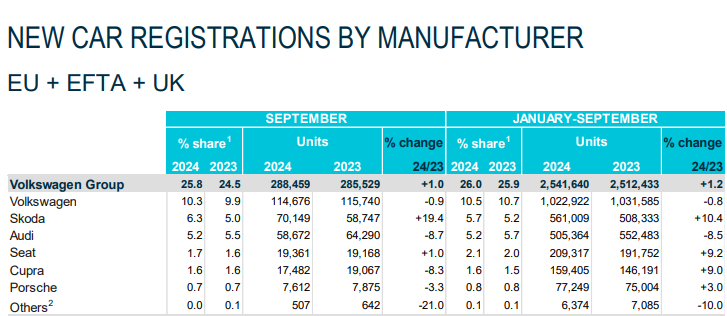

We should also consider insights we get from companies like Volkswagen and provide more context for them.

For example Volkswagen CFO recently said that yearly demand of new cars will be 2 million lower in Europe compared to pre-pandemic. Does this mean he simply expects current demand to remain stable?

I also wonder if Volkswagen sees larger problems coming given their plans to cut jobs or just wants to increase profitability and wonder if this weaker August is meaningful in this context or simply hard yearly comps as you point out.

Yes sure, I am about to finish the first try of GDP and consequent post this week. So, I will most likely be able to continue with this sometime next week.

However, I feel I lack the knowledge and expertise in this sector to fully assess whether long-term structural changes are occurring in sales or not.

But, given the weaker global economy, I don’t anticipate demand to remain that stable. It’s likely they are planning to cut costs as part of risk management? Even if the worst-case scenario doesn’t materialize, this strategy would allow them to improve margins then.

For this, I think I could also use earnings call insgiths from all sectors of the auto industry: manufacturers, dealers, credit institutions, etc, to understand better what they are currently seeing.

Bosch CEO Stefan Hartung told Reuters that Europe is expected to produce a few million cars than forecasted 5 years ago and that it will take a few years for demand to recover.

Bosch is one of the largest autos supplier in Europe with a revenue of €91.6 billion in 2023.

@Magaly have you gotten time to assess how the 2025 sales will develop? I feel like next year will also be a rough ride for automakers mainly due to the 2025 CO2 regulation, rising competition and weaker global economy. Automakers such as the VW brand, Audi brand and others are already increasing prices for the 2025 ICEs and lowering prices for BEVs. That would likely reduce sales for the ICEs.

I am currently working on the sales model, but is still in progress, as I am still gathering data, and researching information for my assumptions. My guess is that it will be ready somewhere in the next couple of weeks (as I usually also have other recurrent macro tasks), and will probably make a post with my assessment.

But from my current knowledge and economic conditions is most likely that yes, I agree that the next couple of years probably be still challenging, especially in Europe and China, with a potential small recovery after that, and with EVs continuing to take market share.

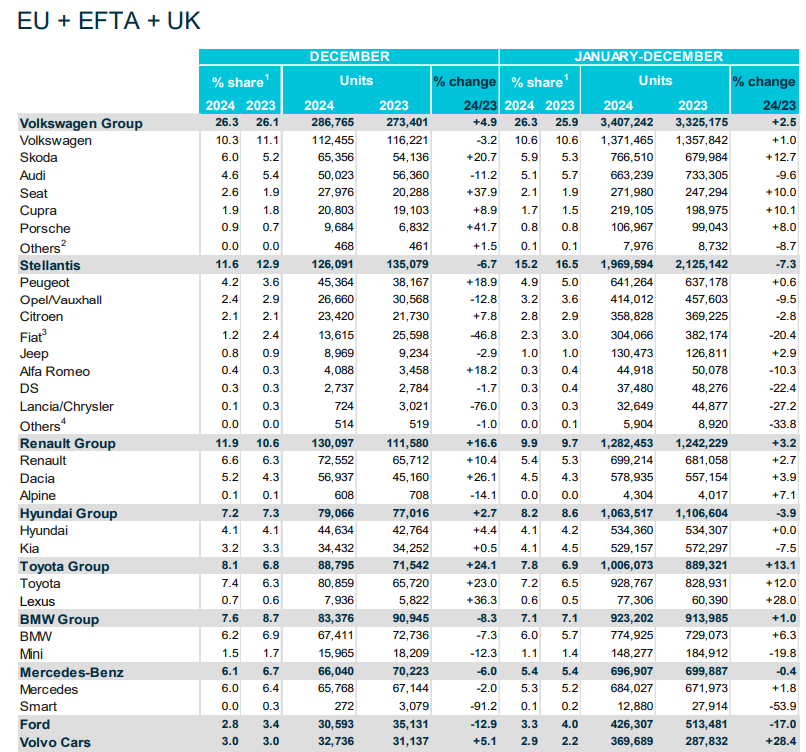

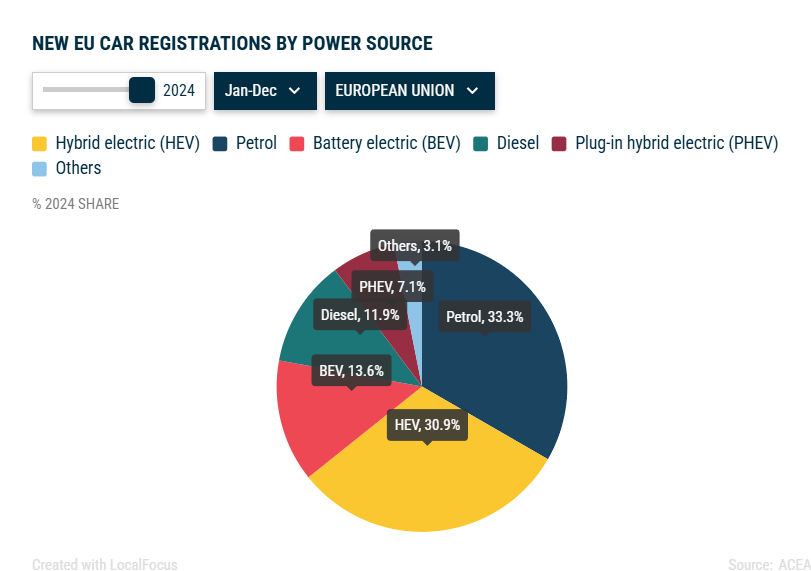

Europe Sales in 2024 were essentially flat. EV sales declined by -1.3%

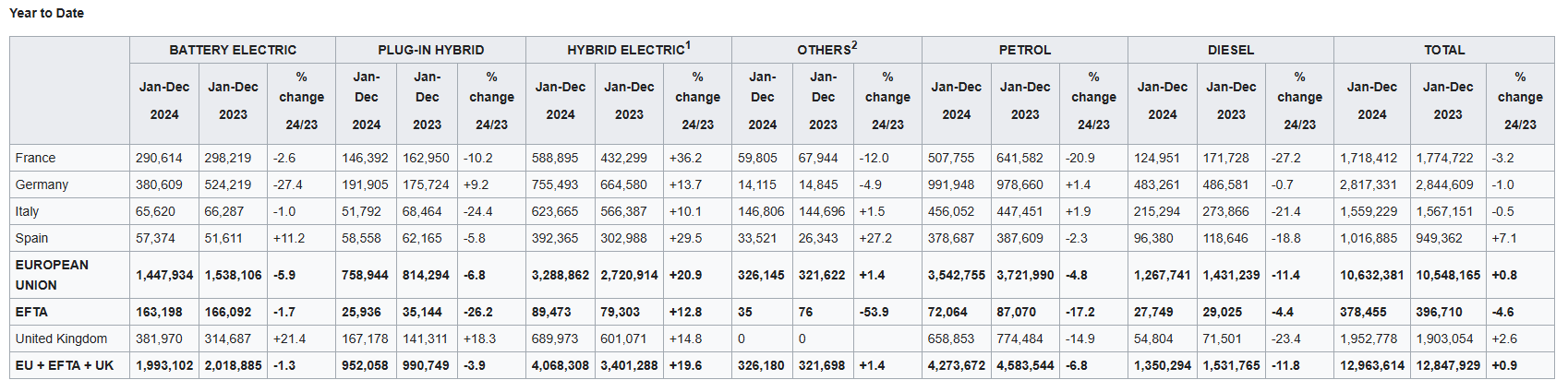

In 2024, new car registrations rose slightly, increasing by 0.9% to around 12.8 million units.

In December, EVs market share stood at 15.9%, contributing to a 13.6% share for the full year down from 14.6% in 2023.

Petrol cars retained their lead at 33.3% (but down from 35.3% in 2023), while hybrid-electric cars strengthened their second position, commanding a 30.9% market share.

ACEA originally expected a 2.5% increase in 2024, so the market performed worse than expected.

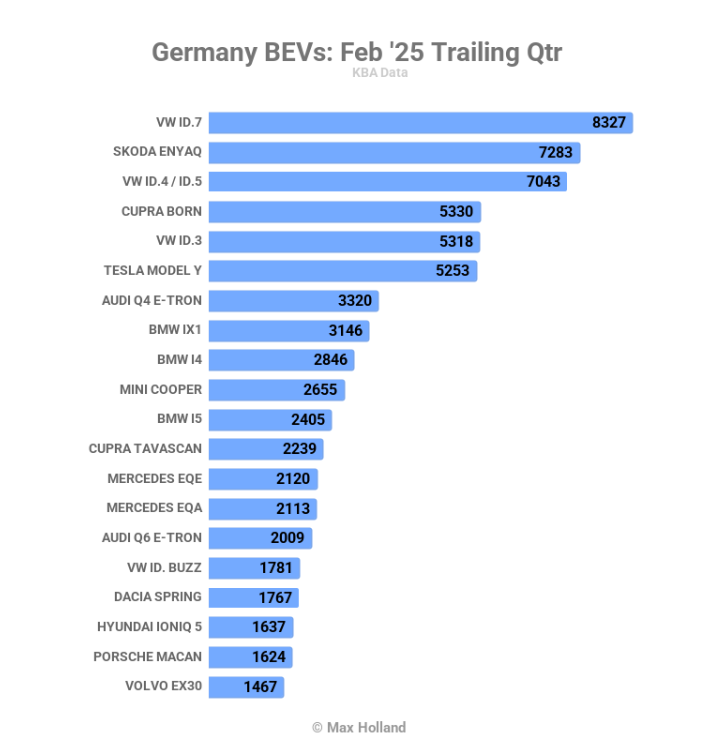

Volkswagen gained 3.4% of the German BEV market share in the trailing 3 months ending in February while BMW and Mercedes lost market share

Volkswagen EVs are doing well in German, according to KBA data. In the trailing 3 months (December-February), Volkswagen took additional 3.4% BEV share in Germany compared to September-November. Six of its BEVs, VW ID.7, Skoda Enyaq, VW ID.4/I.D5, Cupra Born, VW ID.3, and Audi Q4 e-tron were in the top 10 position. BMW lost 2% of the market, Mercedes lost 3.4% while Renault gained 2%.

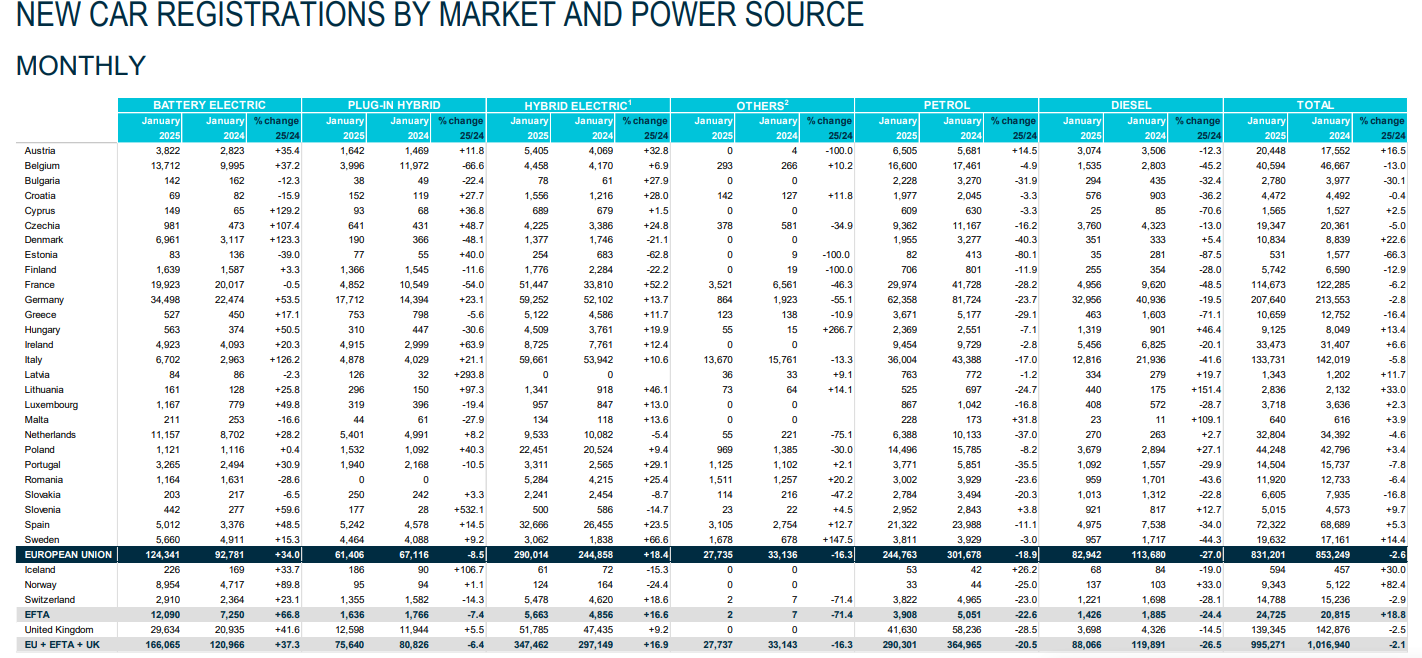

In January 2025, new EU car registrations declined by -2.6%. Notably, the bloc’s major markets saw declines, with France (-6.2%), Italy (-5.8%), and Germany (-2.8%). Spain conversely recorded a 5.3% increase.

In January 2025 , new battery-electric car sales grew by 34% to 124,341 units, capturing a 15% market share

In January 2025 , petrol car registrations saw a significant decline of 18.9%, with all major markets showing decreases.