I=4

Buy, $835: Bofa cited model improvements. It expects the company to release a more powerful model in late 2026 or early 2027. The firm noted progress on Meta’s MTIA processor and visibility on new AI capacity monetization. It added that Meta’s entry into the compute business could provide better visibility on the potential value of Meta’s capacity build.

I=5

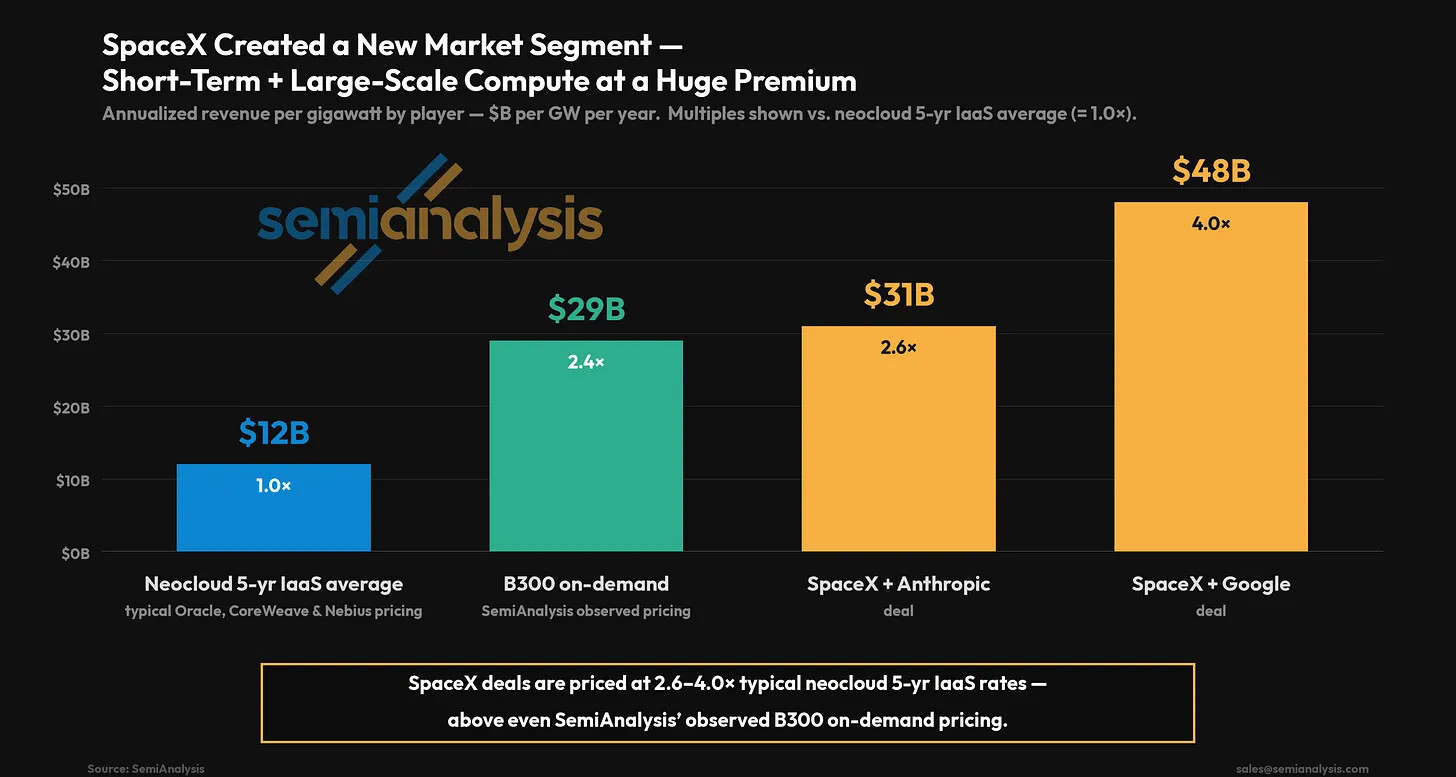

Buy, $930: Evercore’s Mark Mahaney said the most bullish interpretation from the report that Meta plans to launch compute business is that it now has excess compute capacity, reducing the need for further sharp increases in capital spending. He added that this is like the 2022 pivot.

Mahaney pointed out that Meta may have gotten inspiration from Spacex’s deal with Google and Anthropic to supply compute amounting to around $20 billion per year. He doesn’t think that Meta is going after hyperscalers but rather neoclouds.

I=6

Semianalysis projects that Meta’s capex will be “shockingly high” in 2027

-

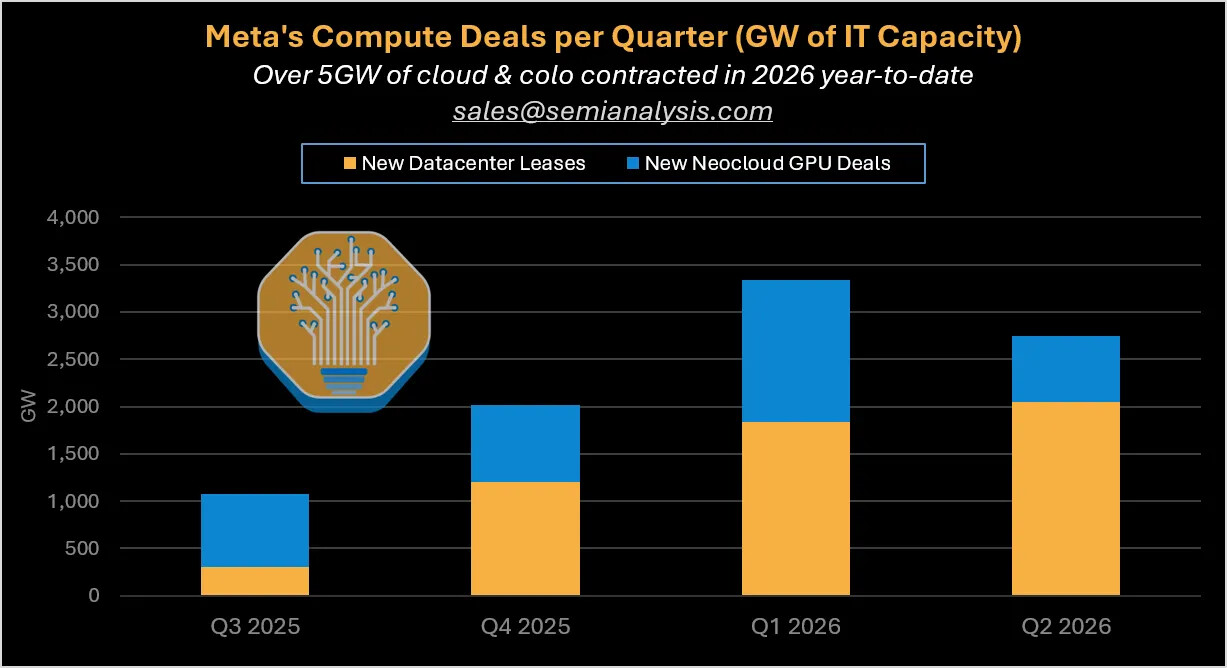

It pointed out that in Meta has contracted over 5GW of capacity in just the first six months of 2026.

-

Drivers of capex include Meta Superintelligence Labs compute needs, assumption that Meta can scale up Ads recommendation systems by over 10x to drive revenue growth, their believe that Meta is in final talks with Anthropic to get access to private instances of Claude in a deal valued at over $10 billion, and expectation that Meta will strike a few “SpaceX-type” deals.

-

Semianalysis pointed out that allocating just 200MW of compute to an external customer drives $10B/yr of revenue, at sky-high margin.

1 Like

I=5

Hold: Needham analayst Laura Martin said Meta’s execution is lagging expectations despite major reorganization and large-scale hiring and infrastracture spending. She interprets the decision to sell cloud services as a sign of underutilized AI capacity. She concludes that future returns on invested capital are likely to decline. She also thinks that gen AI will create “winner-take-most” dynamics, which could distrupt Meta’s leadership position.

1 Like

I=3

Buy, $840: Truist Securities highlighted Meta’s strategy of leveraging its user base to monetize AI, with more than 3.5 billion daily users, 200 million SMBs and over 10 million advertisers. The firm pointed out that it’s monitoring how Meta’s LLMs benchmark against competitors. It views Meta as undervalued and identifies SMBs retooling as a catalyst.

I=5

Overweight: According to Morgan Stanley, Meta’s capital expenditure is projected to increase to $175 billion in 2027 and $205 billion in 2028, up from $145 billion in 2026, driven by the addition of approximately 3.5 GW of capacity in 2027.

The firm believes that Meta will likely persue a Neocloud option rather than Hyperscaler option given it carries low execution risk and less spending.

It pointed out that Meta is expected to add approximately 2 GW of incremental owned-and-operated IT capacity in 2026 and a further 3.5 GW in 2027, building on an estimated 3 GW year-end 2025 base.

It sees Meta leasing out 250 MW for one year at around $40/MW, translating to around $3 incremental EPS in 2028.

I=5

Buy, $800: Wolfe Research said it raised Meta’s 2027 capex to $220 billion versus consensus estimate of $160 billion. It expects Meta will have approximately 17 GW of compute next year, revised upwards from 15 GW. The firm said Meta must demonstrate durable, incremental revenue streams beyond advertising and provide a clear path to returns on invested capital to justify its elevated spending.

I=4

Market Outperform, $825->$800: Citizens lowered price target due to capex concerns and continued execution risks.

I=5

Buy, $835: Bofa said Meta may have achieved significant cost savings in its capacity deployment strategy. It estimates Meta’s 2026 cost per gigawatt at around $22 billion based on $145 billion in capex and 6.5 GW to be deployed. The new cost per gigawatt is below their previous estimate of $45 billoon per gigawatt. Bofa notes that building compute at less than $30 billion per gigawatt could offer favorable economics compared to its estimates for Amazon and Google annual cloud revenues per gigawatt at $10 billion to $16 billion and recently announced SpaceX capacity deals that could range from $40 billion to $50 billion per year per gigawatt.

1 Like

I=6

Outperform, $800: Citizens noted that Instagram engagement momentum continues. It pointed out that global time spent grew 13% y/y in June, marking the thirteenth consecutive month of double-digit growth. U.S. time spent rose 9% y/y, ending a 14-month streak of double-digit growth. Global time spent is facing tougher comps due to strong performance from June last year.

Instagram’s global and U.S. monthly active users are grew 3% y/y and -1% y/y, suggesting Instagram continues to see usage gains from existing members in the double-digits.